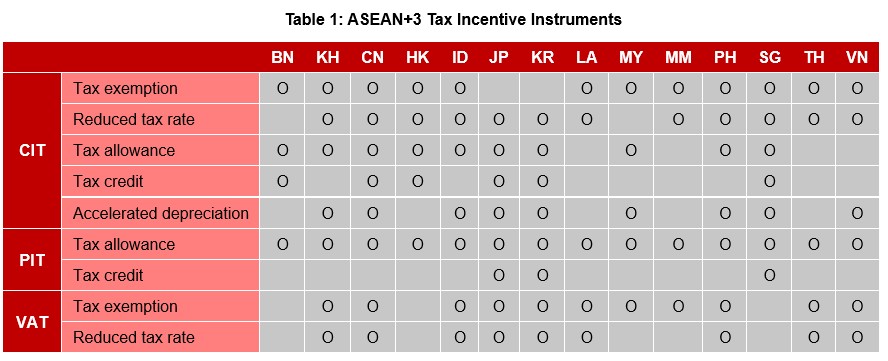

Tax incentives are widely used across ASEAN+3 economies to promote investment and advance policy objectives (Table 1). Among the region’s most widely used measures are corporate income tax (CIT) incentives, aimed at attracting foreign direct investment (FDI), supporting priority industries and special economic zones, and encouraging research and development and innovation. These incentives typically include tax holidays, reduced tax rates, tax allowances, accelerated depreciation, and tax credits. Personal income tax (PIT) incentives—often in the form of allowances—are also widely used to support households and social goals. In addition, value-added tax (VAT) exemptions and customs duty relief are frequently granted for essential goods, education services, and key production inputs.

Source: PwC; Deloitte (2025); EY (2025); AMRO (2025a) Box D; national authorities; AMRO staff compilation

The benefits and costs of tax incentives

When thoughtfully designed and well managed, tax incentives can generate meaningful benefits. They can attract new investment, boost priority sectors, and spur job creation. Beyond these immediate gains, incentives can strengthen supply chains, raise productivity, and stimulate consumption through higher incomes.

However, these benefits come with trade-offs. The most direct cost is forgone government revenue. In some cases, incentives lead to redundant revenue losses when they are granted to investments that would have occurred even without tax breaks.

Complex and preferential tax regimes can also create opportunities for tax avoidance, evasion, and rent-seeking. Over time, this can weaken the tax base, increase administrative burdens, and distort resource allocation, ultimately reducing economic efficiency.

Making tax incentives more effective and efficient

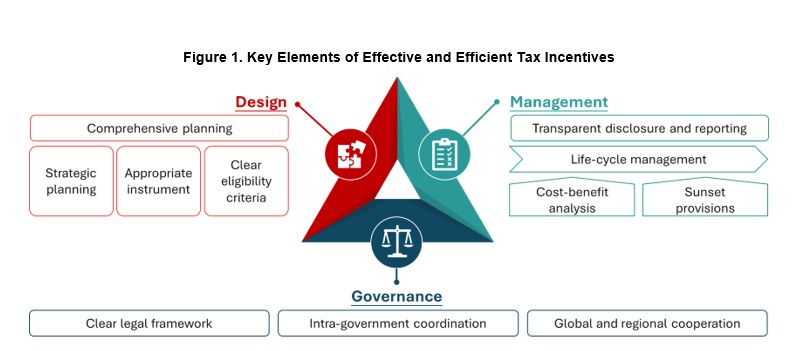

To maximize benefits and contain costs, tax incentives should be anchored in three key pillars: design, management, and governance (Figure 1).

Source: Andriansyah, Hong, and Nam (2021)

1. Design

Effective tax incentives begin with sound design. Incentives should align with a clear national development strategy, and policymakers should assess whether tax incentives are more cost-effective than alternatives such as direct spending or regulatory reforms.

Strategic targeting is equally important. Incentives should focus on sectors or activities that align with national priorities and generate positive spillovers, given their fiscal cost.

The choice of instruments also matters. Cost-based incentives, such as tax credits or allowances tied to actual investments or expenditures, tend to be more effective than profit-based incentives such as tax holidays. As administrative capacity improves, governments should gradually shift toward cost-based incentives.

Clear legal definitions of eligibility criteria further enhance transparency, curtail discretion, and reduce risks of abuse or corruption.

2. Management

Systematic management throughout the life cycle of tax incentives is critical. Transparency is the foundation. Governments should maintain a comprehensive and up-to-date inventory of tax incentives and regularly publish tax expenditure reports to quantify revenue losses. Where resources are limited, a phased approach—starting with major beneficiaries—can be practical.

Life-cycle management is equally important. Tax incentives should not be permanent fixtures. Regular reviews are needed to evaluate effectiveness, with underperforming measures revised or removed.

Ongoing monitoring of beneficiary firms helps ensure compliance and prevent abuse. Cost–benefit analysis should inform both the introduction and removal of incentives. Even where full-scale evaluations are difficult, simplified methods—such as targeted surveys or partial reviews—can still offer valuable insights.

Embedding sunset clauses in legislation is critical. Clear expiry dates help ensure incentives remain temporary and subject to periodic reassessment, rather than automatic renewal.

3. Governance

Strong governance underpins effective design and management. A clear legal framework is essential. Tax incentives should be codified in law, with clear provisions on eligibility, reporting obligations, and evaluation procedures to bolster predictability, consistency, and accountability.

Coordination across government agencies—from finance ministries to investment promotion and sectoral ministries—is vital. Ministry of Finance should lead assessments of fiscal impacts and major approvals, while other agencies contribute sector-specific expertise.

Globally and regionally, cooperation is growing in importance. International initiatives such as the OECD/G20 Inclusive Framework—particularly the global minimum tax under Pillar Two—seek to curb harmful tax competition and profit shifting. At the regional level, ASEAN+3 economies can enhance transparency and policy effectiveness through greater information sharing, more standardizing reporting, and peer learning.

No one-size-fits-all approach

Tax incentive reform is not one-size-fits-all. Each country’s economic structure, institutional capacity, and policy priorities differ. The scope, pace, and sequencing of reforms should therefore reflect national circumstances.

That said, the core principles are clear: stronger design, management, and governance can help ensure tax incentives remain a strategic tool for supporting sustainable and inclusive growth, rather than a costly shortcut.