Discussions about Japan’s public debt often focus on one striking figure: a debt-to-GDP ratio of more than 200 percent. But this number tells only part of the story. Equally important is how financial markets value Japan’s debts—and what that reveals about the country’s longer-term fiscal health as interest rates and investor risk perceptions change.

A recent AMRO analysis helps explain why Japan’s exceptionally high level of debt has not triggered a debt spiral.

Japan’s gross public debt is already exceptionally high by international standards, peaking at about 250 percent of GDP in 2020. The debt ratio is projected to decline in the coming years as pandemic-related spending normalizes. Strong nominal growth and elevated inflation have also improved debt dynamics.

That said, near-term spending pressures remain. Recent measures to cushion the impact of higher energy prices—including energy subsidies, cash transfers, and gasoline tax cuts—could slow fiscal consolidation efforts.

But it is the longer‑run story where the debt narrative shifts. An aging population will continue to push social spending up, while debt servicing costs are expected to rise gradually as effective interest rates increase.

Despite these challenges, Japan’s debt structure provides notable sources of market stability. Japanese Government Bonds (JGBs) have a long average remaining maturity of around nine and a half years. The investor base is also largely dominated by domestic investors, with foreign investors holding around 12 percent of outstanding government securities. In addition, the Bank of Japan (BOJ) remains a major holder of JGBs. Together, these factors reduce the risk of sudden shifts in market sentiment.

A key contribution of AMRO’s analysis is focused on market valuation. The central question is: does the market value of Japan’s debt align with the country’s future fiscal fundamentals?

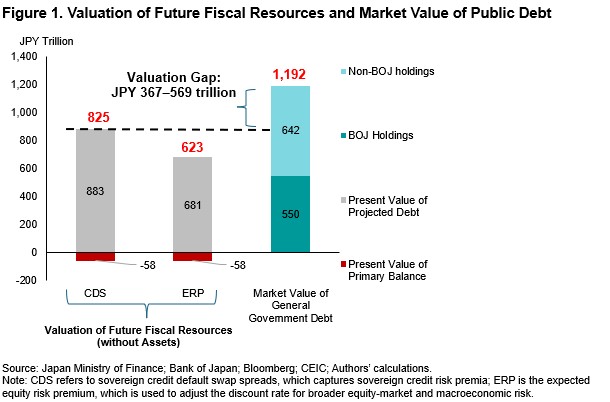

In simple terms, debt should be backed by the government’s ability to generate enough future fiscal resources, which refers to the money it can raise over time after covering regular spending, to repay it. If the estimated value of those future resources is lower than the current market value of debt, it could mean that Japan may need further fiscal adjustment over time, or that investors are currently pricing Japanese government debt more favorably than long-term fiscal fundamentals alone would suggest.

The headline finding is that Japan’s long-term fiscal outlook does not fully cover its existing obligations. AMRO’s analysis points to a significant valuation gap. The estimated present value of future primary balances and terminal debt stock is around JPY 623–824 trillion, a valuation gap of about JPY 367–569 trillion compared with the market value of Japan’s gross government debt of about JPY 1,192 trillion (Figure 1). In other words, projected fiscal resources cover only about half of the market‑valued liabilities. This highlights the scale of adjustment that may be needed to achieve long-term fiscal sustainability.

Could government assets close the gap? Not much, at least mechanically. While the government holds about JPY 788 trillion in assets, less than 10 percent are considered sufficiently liquid in this context. Incorporating those liquid assets does not materially change the valuation comparison.

Still, market pressures have remained contained. One reason is the BOJ’s sizable presence in the JGB market. The central bank holds around JPY 550 trillion in JGBs, which reduces the amount of debt that must be priced and absorbed by private investors. When AMRO compares discounted fiscal flows with the free‑float portion of debt outside the BOJ, the gap narrows considerably (Figure 1).

The broader message is that Japan currently does not face immediate financing stress. The structure of the JGB market— supported by a strong domestic investor base and long debt maturities—remains favorable.

However, as interest rates increase with monetary policy normalization, preserving fiscal sustainability will demand continued consolidation efforts. This will likely require a combination of stronger revenue mobilization, expenditure rationalization, and structural reforms to bolster productivity-led growth.

AMRO’s debt sustainability analysis shows that, without growth‑boosting structural reforms, Japan would need fiscal consolidation averaging about 2 percent of GDP annually between 2033 and 2040. Without fiscal reforms, stabilizing debt would require sustained real GDP growth of around 2 percent per year beyond 2033—a demanding target.

From the market‑valuation perspective, the asset‑pricing results underscore the importance of policy credibility and clear communication. Market valuations are supported when investors remain confident that future fiscal resources will be sufficient to back government liabilities. As the BOJ normalizes monetary policy and adjusts its balance sheet, clear communication on liquidity conditions and policy intentions will be important to reduce the risk of abrupt and disruptive shifts in market risk premia.

Greater transparency around the government balance sheet, especially the liquidity of public assets, could also help investors better assess Japan’s fiscal capacity.

In the end, Japan’s ability to live with very high debt depends heavily on continued market confidence. For now, markets still price Japanese government debt on relatively favorable terms. But if financing conditions tighten and exceptionally low borrowing costs fade, preserving confidence in Japan’s fiscal trajectory will become increasingly important.