The ASEAN+3 region entered 2026 from a position of strength. Yet the energy shock caused by conflict in the Middle East has sharply raised downside risks, making policy flexibility and deeper regional cooperation critical to navigating the uncertainty ahead.

The global economy has barely had time to catch its breath.

Just last year, sweeping tariff shocks disrupted global trade, dented confidence, and forced firms to rethink supply chains. Now, barely months later, a sharp escalation of conflict in the Middle East has delivered the most severe energy shock in decades. Once again, policymakers are navigating a world battered by shock after shock.

For the ASEAN+3 region, the timing matters. The energy shock arrived just as the region was expecting a more balanced risk landscape – and from a position of strength.

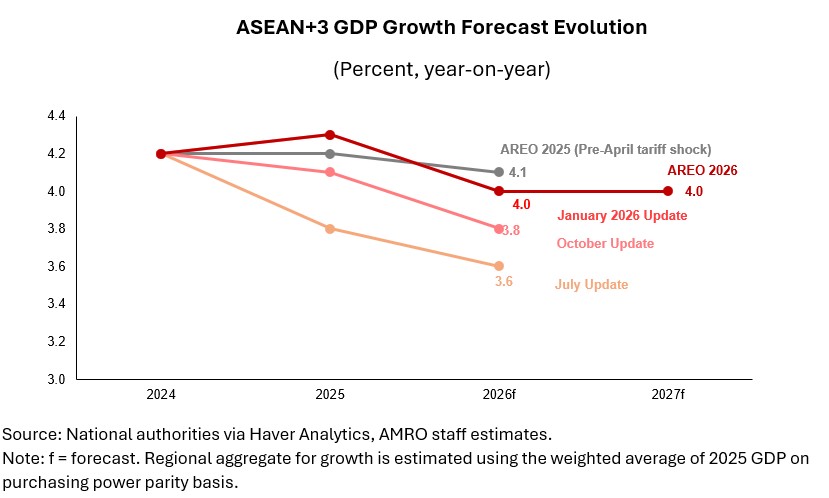

Economic performance across ASEAN+3 surprised to the upside in 2025. Regional growth reached 4.3 percent, well above the 3.8 percent projected in the immediate aftermath of the April tariff shock. Inflation remained low, and external buffers improved. Consumption held up well; exports and investments were buoyed by technology – particularly AI‑driven semiconductor demand.

But strength does not imply immunity.

Energy shocks hit economies through channels that are both immediate and insidious.

Higher oil and gas prices worsen the terms of trade for energy-importing economies, reduce real incomes, and ripple through food prices, services, and manufactured goods. Households cut discretionary spending; firms delay investment. Even as growth slows, inflation rises – energy prices feed directly into headline costs and, over time, broaden into core prices.

This combination – a negative income shock alongside higher inflation – is what makes energy shocks particularly difficult to manage.

Reflecting these dynamics, growth is projected by AMRO to moderate to 4.0 percent in both 2026 and 2027, while headline inflation is expected to rise from 0.9 percent in 2025 to 1.4 percent in 2026 and 1.5 percent in 2027.

These projections assume that oil prices will remain elevated above USD 90 per barrel before easing toward USD 75–85 per barrel in the second half of 2026. They also reflect existing or newly introduced fiscal measures to cushion the impact of the spiking energy costs.

If the conflict escalates and oil prices stay above USD 100, the impact would be far worse. Scenario analysis suggests regional growth could fall by 0.3 percentage points, while inflation could rise by 0.8 percentage points, relative to the baseline.

Even this may understate the damage. A prolonged conflict would trigger cascading and nonlinear effects. Energy shortages would disrupt industrial inputs and spill into petrochemicals, packaging, and fertilizers. Costs would then pass into services and food prices, reinforcing inflationary pressure.

As these channels compound, the total impact could exceed the sum of its parts. This is the nature of a persistent supply shock – it does not stay in one lane. Some economies could also face weaker tourism and remittance flows, while renewed trade tensions or a sharper global slowdown would add further strain.

These risks are real and should not be understated. But the region confronting them today is structurally different from the one that faced earlier energy shocks.

ASEAN+3 today is structurally more resilient. Energy required to produce a unit of GDP has fallen by 20–30 percent since 2000. Power systems have diversified, and electric vehicle adoption is accelerating. These changes weaken the transmission from oil prices to growth – though the current shock has exposed gaps that remain.

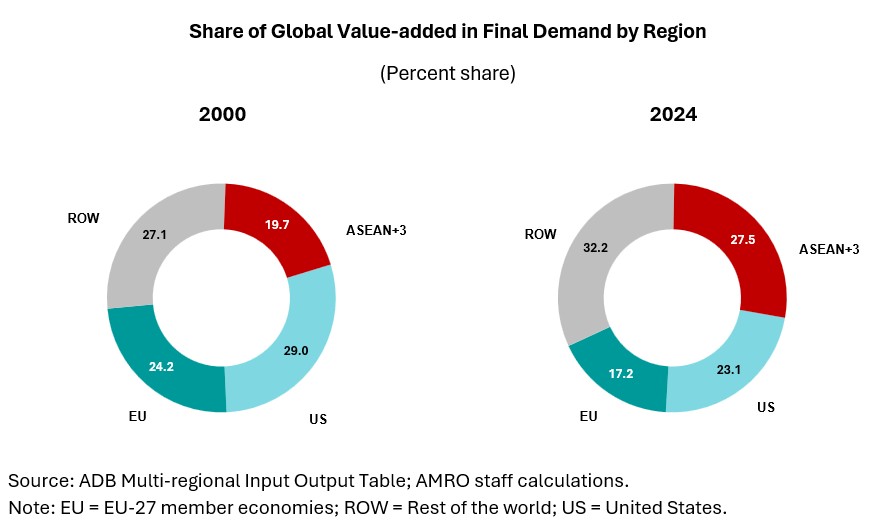

The transformation runs deeper than energy. Over the past two decades, regional production networks have evolved into a dense and sophisticated architecture where the technological capabilities of Japan and Korea, the dynamism of ASEAN, and the scale of China reinforce one another.

On the demand side, ASEAN+3 has emerged as the world’s largest market, accounting for 28 percent of global final demand. The share of value‑added exports absorbed within the region has risen to nearly 30 percent, while reliance on the United States has declined to around 20 percent.

Against such a changed structural background, the central policy priority in the short term is to avoid worst-case outcomes such as stagflation. Most ASEAN+3 economies retain meaningful fiscal and monetary space – and the imperative now is to preserve that flexibility, given the elevated uncertainty and the unusually wide range of plausible outcomes.

Monetary policy should remain supportive of growth while responding flexibly if price increases broaden into core inflation or risk unanchoring expectations. Preserving orderly market conditions and financial stability remains essential.

Fiscal policy has a complementary role. Targeted support for vulnerable households and exposed sectors can help cushion the real income shock. What should be avoided are broad based price suppression measures that could undermine fiscal sustainability.

Above all, responses must remain state contingent. The nature and persistence of the shock – not its headline severity – should determine the policy stance.

Looking beyond the short-term, the energy shock underscores that the green transition is critical to macroeconomic resilience. Diversifying energy and input sources, accelerating electrification, strengthening strategic reserves, and keeping regional trade open are not separate priorities – they are elements of a single resilience strategy.

Deepening regional cooperation remains ASEAN+3’s strongest collective asset. For ASEAN, this means moving beyond trade liberalization to build denser intraregional investment links and a more balanced, resilient production base.

The path ahead will test these foundations in real time. But if policymakers preserve their flexibility, maintain fiscal discipline, and continue to deepen the cooperation that underpins the region’s collective strength, ASEAN+3 is well positioned to navigate this shock – and emerge more resilient for what comes next.