A version of this article was published in The Edge Malaysia on April 21, 2026.

The Middle East conflict is placing ASEAN+3 under immediate economic pressure. But its deeper significance may lie in what it leaves behind for the region’s longer-term resilience and competitiveness.

The immediate economic consequences of the Middle East conflict remain front and center. Energy prices have risen, transport and logistics have come under pressure, and the risks to inflation, external balances, and confidence have become more acute. But the more important question may lie beyond the first shock: not only how the disruption is managed today, but what it may leave behind once the immediate pressures begin to ease.

That question matters now, not later. By the time the longer-run implications of a shock become obvious, many decisions have already been made — by firms adjusting supply chains, by investors reassessing risk, and by governments rethinking exposure and preparedness. Looking further ahead is therefore not a distraction from managing the present. It is part of managing it well.

For ASEAN+3 – ASEAN together with China, Japan, and Korea – this is not a peripheral issue. It is a region where energy dependence, trade intensity, manufacturing linkages, maritime connectivity, and external financing are closely intertwined. Shocks rarely arrive through a single channel. They move through fuel costs, freight, insurance, exchange rates, finance, industrial inputs, and production systems at the same time. That is why the current conflict is not only an energy shock. It is a reminder that a highly open and deeply networked regional economy can be exposed in broader ways than headline oil prices alone would suggest.

The case for looking further ahead is not that the future is already clear. It is not. The more modest point is that some shocks leave a wider legacy than first appears. The oil shocks of the 1970s left behind an enduring architecture of energy security. After 9/11, global trade did not retreat, but the way it was secured changed in durable ways. The pandemic altered how firms changed inventories, supplier strategies, and the way supply chains were managed. Europe’s response to the Russia-Ukraine conflict similarly went beyond absorbing higher energy prices to rethinking sourcing, infrastructure, and exposure.

The lesson is straightforward: major disruptions often leave behind broader changes in policy frameworks, production systems, and how resilience and competitiveness are defined.

For ASEAN+3, that possibility is especially important because the region’s strengths and vulnerabilities are closely connected. The same openness that supports growth and regional integration can also transmit disruption quickly when energy, logistics, and finance come under stress simultaneously. But that is only one side of the story. If firms and investors place greater weight on continuity, reliability, and the ability to operate under stress, then the issue is no longer only vulnerability. It is also whether parts of ASEAN+3 can strengthen their position as resilient and dependable production bases in a more uncertain world.

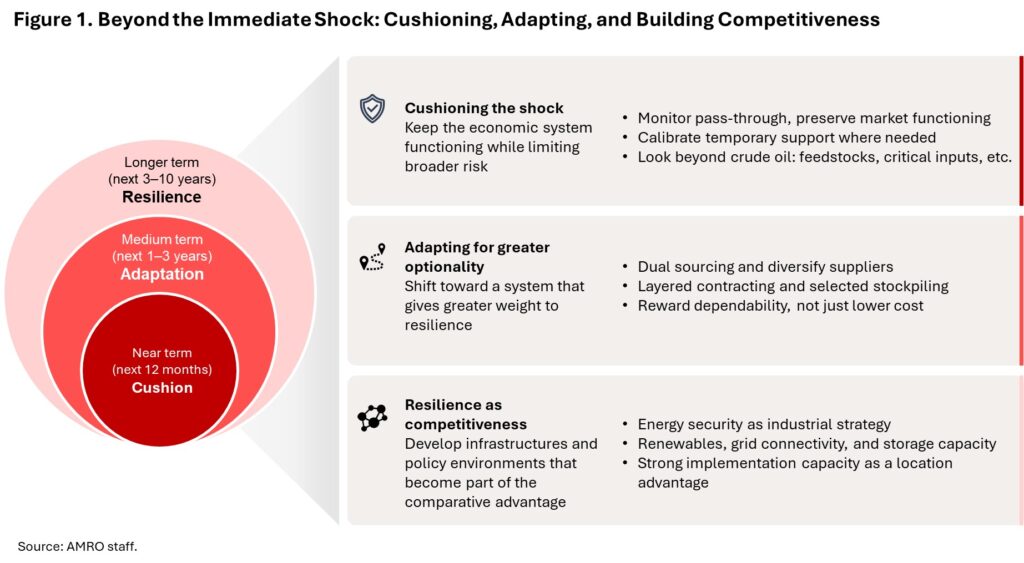

Resilience, in this context, should be understood more broadly than stockpiles. It is often reduced to reserves, particularly crude oil reserves. But resilience has at least three dimensions: absorbing disruption through buffers such as reserves, inventories, and fiscal space; adapting through rerouting, substitution, coordination, and recovery under stress; and remaining competitive by offering continuity when disruption occurs.

For ASEAN+3, this broader view matters because exposure extends beyond crude oil to LNG, petrochemical feedstocks, shipping and insurance, ports, customs, payments, reliable power, and the production networks that connect them.

Seen in this light, the policy challenge spans three overlapping horizons (Figure 1). In the near term, the priority is cushioning – keeping the systems functioning and preventing temporary disruptions from becoming broader macroeconomic stress. In the medium term, the focus is adaptation – building more fallback options through diversification, strengthening inventories for selected vulnerabilities, better route planning, and improving operational resilience. Over the longer term, the issue becomes more strategic – whether resilience is built into the foundations of competitiveness itself. In that sense, it is no longer solely a question of risk management, but increasingly one of industrial policy.

This also has implications for macroeconomic surveillance. A world of deep uncertainty and multi-channel shocks requires more than extending baseline forecasts a little further outward. The most consequential risks may not appear first in the central scenario. That is why surveillance needs to rely more on scenario analysis, horizon scanning, and strategic foresight –not to displace the baseline forecasts, but to test them and to ask what could matter materially if conditions worsen, through which channels those pressures would propagate, and what policy trade-offs might then come into view.

This also points to where future work should go. As the region looks beyond the immediate shock, greater attention will need to be given to resilience beyond crude oil alone – across energy systems, maritime logistics, critical industrial inputs, and the analytical tools needed to monitor them. This is not about overstating the implications of a single conflict. It is about avoiding the narrower mistake of treating the shock as purely a temporary macroeconomic disturbance and postponing the deeper questions until the next disruption exposes the same vulnerabilities again.

ASEAN+3 still needs to manage today’s shock carefully. But that is not a reason to postpone thinking about what comes next. It is the reason to begin now.