Despite being an advanced economy with deep financial markets and globally competitive industries, Korean equities have persistently traded at a significant discount to global peers – a phenomenon widely known as the “Korea Discount”.

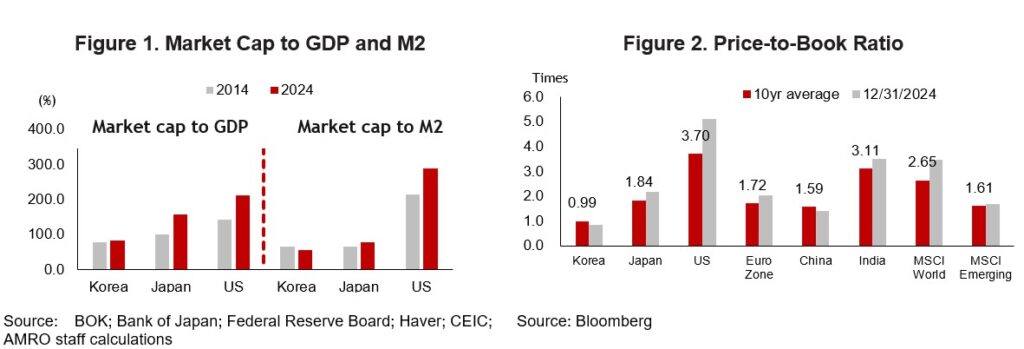

Over the past decade, Korea’s market capitalization relative to GDP has remained stagnant, while those of major markets such as the US and Japan have grown significantly (Figure 1). The average price-to-book ratio (PBR) of the benchmark KOSPI index has hovered around 0.99 – well below that of advanced and emerging market peers (Figure 2). In effect, a large share of Korean listed companies continues to trade below book value, suggesting that the market values them less than the net assets.

Structural factors behind the discount

Several structural factors have contributed to this gap. Corporate profitability has been comparatively subdued, with average return on equity (ROE) hovering around 7 percent over the past decade. While not weak in absolute terms, this has generally been insufficient to command premium valuations.

Corporate governance concerns have also weighed on sentiment. These are most often associated with conglomerate‑affiliated firms – the chaebol groups – where controlling shareholders have historically exerted considerable influence, at times to the detriment of minority shareholders. In addition, shareholder returns have remained modest by international standards, with relatively low dividend payout ratios.

The cumulative effect has been a gradual erosion of investor interest in Korean equities, both domestically and internationally. Also, domestical capital increasingly shifted toward real estate, raising concerns that the equity market was not fulfilling its role in allocating capital efficiently and supporting economic dynamism. In response, the authorities launched a multi-pronged reform agenda.

Combining corporate engagement with market infrastructure

Partly inspired by Japan’s experience, Korea introduced the Corporate Value-Up Program in 2024, encouraging listed companies to voluntarily formulate and disclose plans to enhance corporate value. In Japan, persistent concerns over weak capital profitability—reflected in widespread ROEs below 8 percent and PBRs below 1—prompted the Tokyo Stock Exchange in 2023 to call for management reforms focused on capital efficiency and corporate value. That initiative is widely seen as helping catalyze Japan’s subsequent equity market rally.

Korea’s approach combines corporate engagement with market infrastructure. Authorities have provided incentives to encourage participation and introduced the Korea Value-Up Index and related exchange traded funds (ETFs) to broaden the investor base and promote more stable, long-term capital inflows.

Legal reforms have reinforced these efforts. Amendments to the Commercial Act have strengthened shareholder protection and improved governance transparency. More recently, a requirement to cancel treasury shares was introduced to further enhance shareholder returns and limit their use by controlling shareholders.

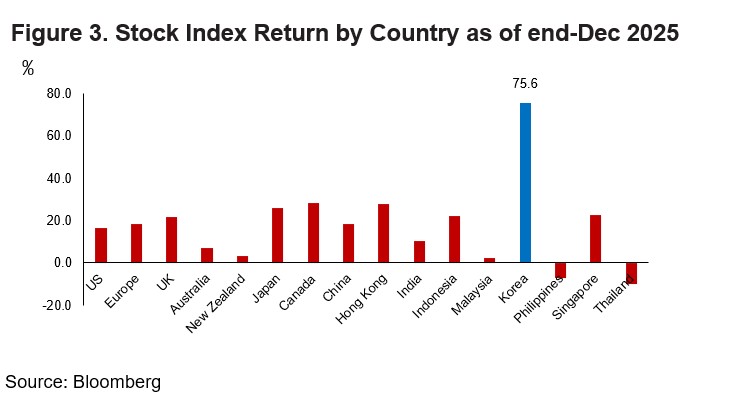

Early results are encouraging. Since mid-2025, foreign capital inflows into Korean equities have picked up, and the KOSPI has been among the stronger-performing global equity markets (Figure 3). Shareholder return indicators have also improved, with dividends and share cancellations rising steadily.

Challenges and the way forward

The recent momentum is welcome, but important caveats remain. Despite headline gains, a large share of Korean firms still trade below a PBR of 1, while more than 60 percent record ROE below the long-term average of 7 percent. Moreover, the rally has been narrowly concentrated: Samsung Electronics and SK Hynix together accounted for about half of the total increase in KOSPI market capitalization in 2025. Excluding these two semiconductor heavyweights, the recovery appears considerably more modest.

More fundamentally, stronger equity valuations have yet to translate into improvements in employment or domestic demand. Gains in corporate fundamentals have not yet taken hold across the broader economy.

For the Value-Up Program to deliver lasting benefits, reform efforts need to deepen and broaden. Three priorities stand out.

First, policies should focus on sustained improvements in corporate profitability and capital efficiency. This includes encouraging firms to restructure or divest low-return, non-core businesses and strengthening governance frameworks to ensure ROE improvements are structural rather than cyclical.

Second, stronger institutional foundations are needed to ensure that rising equity valuations support real economic activity. A more vibrant capital market should support higher corporate investment and job creation, particularly in innovative and high-growth sectors. Well-targeted financial support, tax incentives, and regulatory reforms can help channel capital toward productive uses.

Third, more effective exit mechanisms for unproductive firms are essential. Without stronger market discipline, inefficient capital allocation will persist, undermining investor confidence and limiting the broader impact of reforms.

Implications for the region

The success of these domestic efforts carries weight far beyond Korea’s borders. As Korea strives to dismantle the “Korea Discount,” its journey is becoming a blueprint for a wider regional trend. Indeed, Korea’s Value-Up reform is not an isolated experiment but part of a shifting paradigm in regional capital markets.

Just as Japan’s earlier corporate governance initiatives served as an important reference for Korea, the reform momentum is now spreading further. Singapore’s recent “Value Unlock” program, for instance, echoes these efforts by encouraging listed companies to strengthen investor engagement and enhance shareholder value.

These parallel initiatives carry broader significance for the ASEAN+3 region. Economies that move decisively to improve corporate governance, strengthen shareholder returns, and deepen capital markets will be better positioned to attract investment, foster innovation, and sustain economic growth.