At first glance, stablecoins appear simple: one token equals one unit of fiat currency, typically US$1. Issuers generally claim each token is backed by safe assets and can be redeemed at par under specified terms. The assumption seems straightforward—if reserves are sound, the token should remain stable.

Yet, this view captures only part of the story.

For most users, stability is not determined solely by the quality of reserves. What matters is whether stablecoins can actually be converted into fiat currency at the expected value, when needed, and without disruption. That depends on trading conditions, intermediaries, and payment channels—the infrastructure, or market plumbing, that enables users to exit their positions.

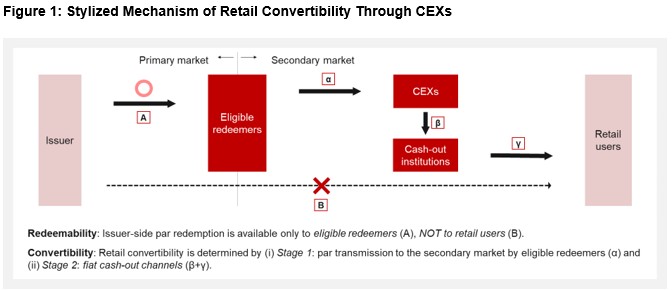

Redeemability versus retail convertibility

The path from stablecoin to fiat typically involves a two-layered market structure:

Primary market. This is where issuers create and redeem tokens. However, direct access is usually limited to a select group of eligible participants, such as institutional investors, or large counterparties that meet minimum transaction thresholds.

Secondary market. Most users buy and sell stablecoins mainly through centralized exchanges (CEXs) (Figure 1). This is where ordinary users sell and convert tokens into fiat, often relying on banks or payment service providers.

Put simply, eligible redeemers use the primary market to redeem stablecoins at par, while most users rely on the secondary market to convert them into usable fiat money.

The distinction matters because redeemability and retail convertibility are not the same.

Redeemability refers to the issuer’s contractual commitment that allows eligible participants to return stablecoins and receive fiat at par value, subject to the issuer’s terms and conditions.

Retail convertibility, by contrast, refers to the practical ability of ordinary users to obtain fiat through available channels, factoring in price deviations, delays, withdrawal constraints, and payment frictions.

A stablecoin may be redeemable at par for a limited group of participants while ordinary users experience discounts, delays, or restricted access in practice. Even when reserves are sound, weak retail convertibility can undermine confidence because most users experience stability through secondary market conditions rather than direct redemption.

Where convertibility can weaken

Retail convertibility can weaken at two critical stages.

First, par transmission. While eligible redeemers may obtain par value directly from issuers in the primary market, most users rely on secondary markets. When prices fall below par, arbitrage can, in theory, restore alignment. Arbitrageurs may purchase discounted tokens and redeem them with issuers at par—helping the secondary market price go back toward par.

In practice, however, arbitrage is not automatic. Its effectiveness depends on redemption access, processing speed, and arbitrageurs’ capacity and confidence. If arbitrage becomes constrained, the issuer’s par anchor may remain intact, but market prices can still diverge, leaving ordinary users to face a worse price.

Second, fiat cash-out. Even after stablecoins are sold, users still need to receive fiat funds through banking and payment systems. Stablecoins may move across blockchains continuously, operating around the clock. Fiat systems, however, often depend on banking hours, settlement schedules, and payment cut-off times.

This timing mismatch becomes particularly important during periods of stress. Weekends, public holidays, banking disruptions, or payment systems outages may constrain access to fiat liquidity. Under such circumstances, stablecoins may temporarily trade below par if immediate access to cash becomes scarce or uncertain.

Together, these frictions suggest that stablecoin reliability depends not only on reserve assets but also on the resilience of the mechanisms that enable users to convert holdings into fiat.

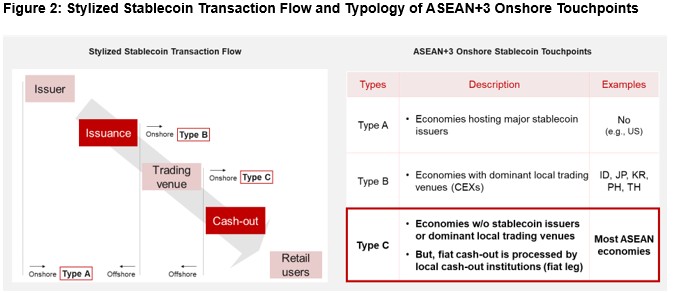

The importance of onshore touchpoints

The two-stage process highlights not only where retail convertibility can weaken, but also shows where domestic authorities may have practical leverage (Figure 2).

This is especially important for ASEAN+3 economies, many of which are not stablecoin issuance centers. Domestic authorities may have limited visibility into offshore issuers or direct control over reserve management. However, they often retain oversight over domestic exchanges, payment service providers, banks, and other local intermediaries that facilitate conversion between stablecoins and fiat. These are enforceable onshore touchpoints.

Requirements can be attached to these touchpoints. Exchanges can be required to report whether trading remains orderly. Cash-out routes can be monitored for whether users actually receive fiat, and how long the process takes.

This shifts the regulatory focus beyond reserve backing alone toward understanding how stablecoins intersect with domestic financial systems and payment infrastructure.

Regulatory implications

Once these domestic touchpoints are identified, regulatory responses can be tailored according to policy objectives and the characteristics of different digital instruments.

For permitted local currency digital instruments, stricter standards around cash-out reliability may be justified given their closer integration with domestic financial systems. For foreign currency stablecoins, the policy challenge is different. Authorities may need to contain risks without pushing activity into less visible or unregulated channels. A practical approach is to keep key conversion and cash-out points within regulatory reach, and to attach clear safeguards, reporting requirements, and contingency arrangements where they are justified by domestic policy objectives.

For ASEAN+3 economies, this framework may prove particularly relevant. Offshore foreign currency stablecoins are likely to circulate regardless of whether domestic authorities actively support them, while future local currency digital instruments may warrant different forms of oversight. In this context, effective regulation may require looking beyond issuer’s balance sheets toward the broader ecosystem that shapes how users access and exit stablecoin markets.

Stablecoins are more than reserve portfolios. They are arrangements that depend on market incentives, intermediaries, and payment rails to function smoothly. If stability is ultimately judged by users’ ability to convert tokens into fiat when needed, regulation should follow the full journey—from issuance to cash-out.