For decades, the ASEAN+3 region has been the powerhouse of global economic expansion, contributing over 40 percent of the world’s GDP growth. Today, however, this engine has weakened and is slowing. The vibrant growth that once defined the region has steadily declined since the global financial crisis, further eroded by the COVID-19 pandemic, and faced with several structural challenges and risks in the period ahead.

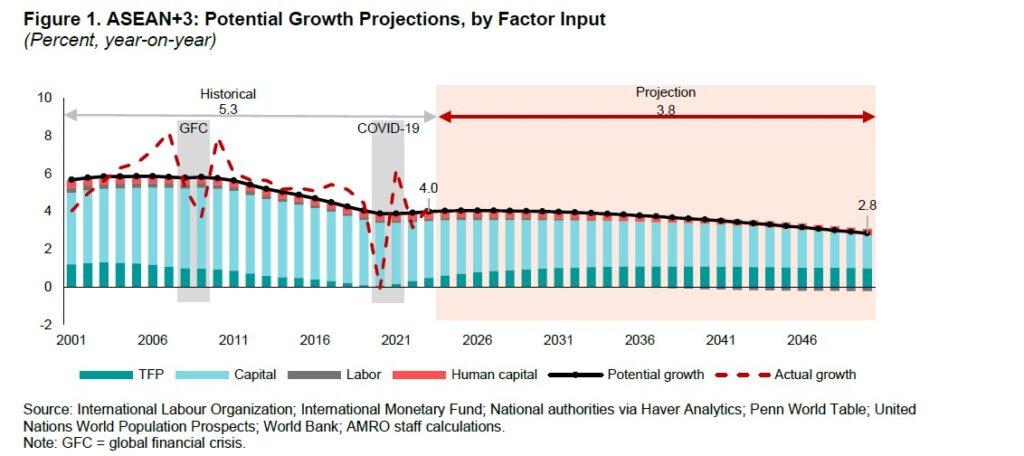

AMRO’s analysis reveals a sobering trajectory: potential growth in the region has declined from 6.0 percent in the early 2000s to 4.0 percent in 2023 (Figure 1). The causes for the slowdown in potential growth are clear. Approximately 70 percent of this decline stems from slower capital accumulation, while sluggish total factor productivity (TFP) accounts for another 10 percent. In several economies, slow human capital development and shrinking labor forces are also a drag on potential growth.

Of greater concern, projections suggest a further decline to about 3.0 percent by 2050, or even lower if downside risks such as a more drastic fall in fertility rates and severe geoeconomic fragmentation, were to materialize. This is not merely a cyclical downturn but a structural challenge demanding urgent and strategic policy actions.

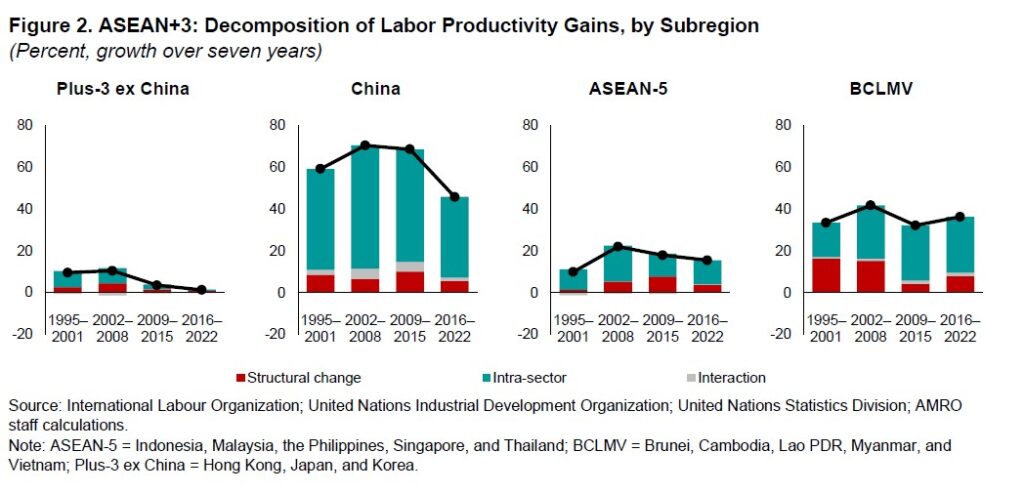

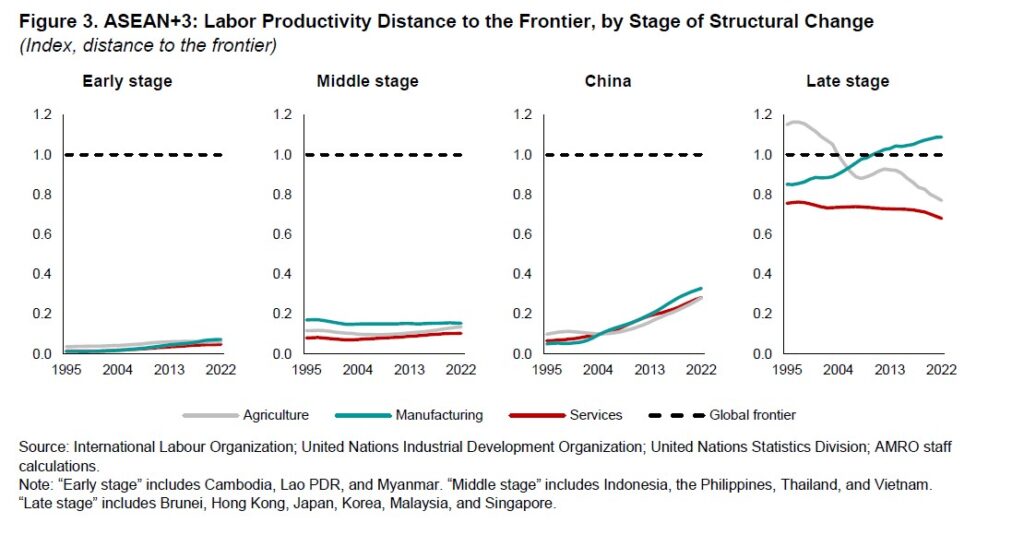

While the dynamics vary across economies, successful transitions to higher-income status have historically relied on a combination of rapid capital accumulation, strong productivity growth, and human capital development. Yet, productivity gains from structural change have fallen in most of the subregions after the global financial crisis (Figure 2). Industrialization has stalled in some economies in the middle stage of structural change, and sectoral productivity gaps compared to global frontiers remain stubbornly wide (Figure 3). Although the sectoral productivity gaps are closing for China, they remain relatively large. Moreover, the shift toward services has mostly been concentrated in lower productivity segments.

The challenge now is not just to reignite growth, but to revitalize it. This calls for bold, transformative strategies that harness the region’s strengths while addressing its vulnerabilities.

Five key policy priorities can guide ASEAN+3 economies toward a stronger, more sustainable and inclusive growth path.

First, the region must upgrade manufacturing capabilities to respond to new technological advances and demand dynamics. Rather than moving away from manufacturing – still a critical driver of productivity growth – ASEAN+3 economies should embrace the rapidly evolving value chains, including those linked to green transition while embracing new technologies to enhance productivity.

Second, a deliberate shift toward high-skills services is essential. The manufacturing and services sectors are increasingly intertwined. A shift toward high-value services can drive productivity and job creation, especially as global manufacturing evolves with technological advances.

Third, closing investment gaps must be prioritized, particularly in productivity-enhancing infrastructure. Over the next two decades, the region faces infrastructure investment gap totaling approximately USD 1.9 trillion. Investment must also focus on enhancing human capital, and developing sectors and skills that are aligned with global demand to complement physical infrastructure improvements and amplify its economic impact.

Fourth, innovation and technology adoption must be prioritzed. Innovation and technology adoption are key to improving resource allocation and protecting ASEAN+3’s growth momentum against secular decline. Economies can also speed up structural transformation by leveraging advances in new technology, especially artificial intelligence.

Finally, the state capacity for policy design and implementation must be strengthened. Even the most well-designed policies will fail without effective implementation. Governments must invest in technical expertise, strengthen transparency and accountability, and improve inter-ministerial and intergovernmental coordination to ensure successful policy delivery.

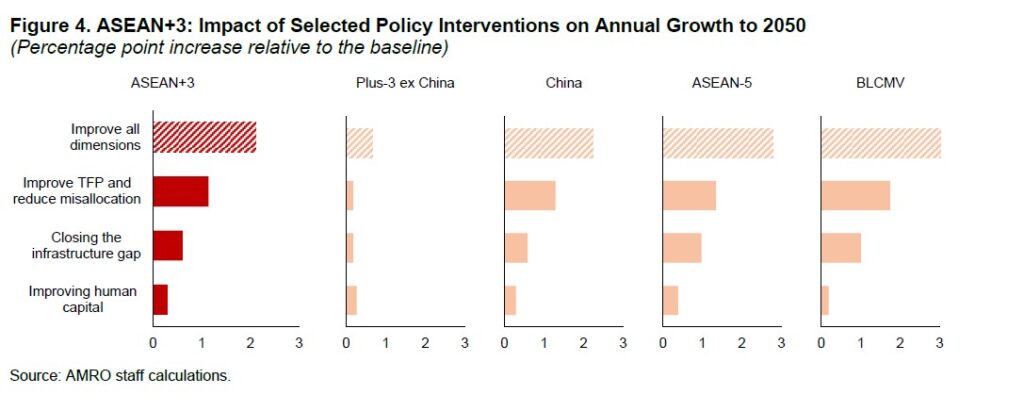

The rewards of successful transformation are substantial. AMRO’s scenario analysis shows that ASEAN+3 growth could be more than 2 percentage points higher on average over the next decade relative to the baseline projections if the authorities are able to improve productivity, close investment gaps, and enhance human capital (Figure 4).

Furthermore, deeper regional cooperation can ease the massive investments required, especially by the early and middle-stage economies. The more advanced economies and China should invest in other economies to leverage the complementaries of economies. Collective action in areas such as cross-border logistics, climate resilience, and productive aging can yield greater returns than national efforts.

The ASEAN+3 region’s economic success over the last several decades was a miracle that was built on bold policy choices, effective implementation, and an ability to adapt to changing circumstances. Today’s challenges require that same level of leadership and vision. By charting new growth pathways, the region can reinvigorate economic development that is not only dynamic but also inclusive, equitable, and sustainable.