This article was first published in The Phnom Penh Post on February 4, 2024.

Maintaining confidence in banks serves as a crucial step in building up the resilience of a country’s financial system and macroeconomy, particularly in developing economies. In this context, a deposit insurance system, guaranteeing the repayment of client deposits within a ceiling when a contributory bank fails, plays a pivotal role in helping banks to bolster consumer confidence by protecting depositors and reducing the risk of bank runs (IADI’s Core Principles).

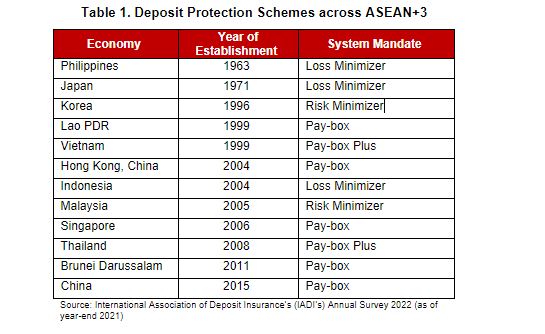

Countries across the ASEAN+3 region recognize the benefits of having such a safeguard and most of them have in place an explicit deposit protection or insurance scheme (Table 1). Their schemes differ depending on mandate (and coverage). Several countries narrowly define the mandates of deposit insurers, focusing on the reimbursement of insured deposits (“Pay-box”) or incorporating specific resolution mechanism (“Pay-box Plus”). Countries such as the Philippines, Japan and Indonesia grant deposit insurers the authority to pursue a variety of resolution strategies (“Loss Minimizer”). In Korea and Malaysia, deposit insurers adopt a more comprehensive risk minimization approach and take into account risk assessment and management (“Risk Minimizer”).

Cambodia is one of the few countries in ASEAN+3 that does not have a deposit protection scheme. The time is ripe for one to be established.

Sizable financial system

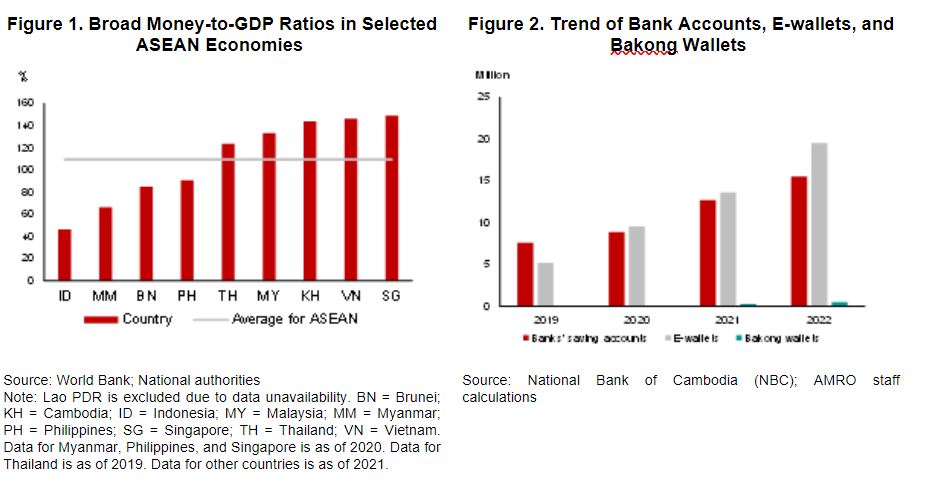

First, establishing a deposit protection scheme will help strengthen Cambodia’s financial sector, which has grown even faster than its economy. Broad money circulation, largely comprising deposits, surged from 41.6 percent of GDP in 2010 to 142.1 percent in 2022, making it one of the three ASEAN countries with the highest broad money-to-GDP ratios (Figure 1).

Cambodia’s banking landscape is predominantly characterized by depository institutions. From a financial stability perspective, it is crucial not only to protect the large banks, which hold 68 percent of the deposits, but also to safeguard the smaller ones. Even the collapse of a small bank can undermine consumers’ confidence, potentially triggering bank runs.

Last year, the collapse of the Silicon Valley Bank in the U.S. was, in part, the result of a classic bank run. Depositors, fearing insufficient funds, withdrew their deposits, which triggered a chain reaction that also led to the failure of Signature Bank and Silvergate. The bank runs prompted the U.S. Federal Reserve and the Federal Deposit Insurance Corporation to announce measures to protect depositors, which helped to restore depositors’ confidence in the banks and avoid further bank runs. This incident highlights the importance of deposit protection schemes to mitigate the risk of a bank run to an economy.

Rapid financial digitalization, high level of dollarization

Second, the rapid digitalization of financial services in Cambodia underscores the urgent need for regulators to take measures to address potential digital bank runs. The expansion of fintech in Cambodia has made formal financial services more accessible and at lower costs. Higher financial inclusion also means an increase in risk.

The total volume of electronic payments in Cambodia surged from USD 85 billion in 2019 to USD 274 billion in 2022, almost 10 times the size of GDP. The number of completed transactions increased to 1 billion in 2022 compared to 708 million a year ago. Digital accounts, including e-wallets with Cambodian banks, have also witnessed remarkable growth, from 5.2 million in 2019 to 20 million in 2022 (Figure 2).

The growth of digital financial services may lead to higher risk of bank runs and greater financial instability in the event of a shock to the financial system. Recent research on historical banking crises revealed a stark shortening of depositors’ withdrawal period over the years (Rose, 2023).

During the Global Financial Crisis, this period increased from 16 to 19 days. With the advent of digital banking, this period has been dramatically reduced to under just two days, stressing a pertinent need for regulators to take measures to address potential digital bank runs.

Third, Cambodia’s significant level of dollarization highlights the importance of establishing foreign currency funds as the first line of defence to protect foreign currency deposits. Since most deposits in Cambodia are in U.S. dollars, the National Bank of Cambodia (NBC) cannot fully perform its role as the lender of last resort by injecting USD liquidity into a bank when there is a bank run. This could further undermine public confidence during a crisis. With the establishment of the deposit protection scheme, participating financial institutions will contribute a premium to the scheme annually. The funds from such premium contribution will grow over the years and can be utilized to address potential bank runs.

Simulation exercises carried out as part of AMRO’s 2023 Annual Consultation Report on Cambodia showed that with appropriate premiums and coverage limits, a deposit protection scheme can be designed to provide limited protection to depositors in the event of insolvency of small banks by guaranteeing the repayment of deposits up to a ceiling.

Protect local and foreign currency-denominated deposits

One of the biggest issues when introducing DPS in Cambodia is whether to provide protection for foreign currency-denominated deposits. As around 90 percent of financial institutions’ deposits in Cambodia are in U.S. dollars, providing deposit protection only for local currency deposits would be insufficient. For this reason, several highly dollarized countries in South America offer protection for foreign currencies as well as their local currencies.

However, protecting foreign currency deposits can hinder efforts to promote the greater use of the local currency. It may also put more pressure on foreign reserves, which are needed for the deposit protection scheme to guarantee foreign currency deposits. It is therefore imperative to balance the goals of promoting the local currency while protecting foreign currency deposits at the same time.

The set-up of an internal Deposit Protection and Bank Resolution Unit by the NBC to conduct a feasible study on the establishment of a deposit protection scheme is an important first step. In particular, a working group on deposit protection mechanism led by the NBC and including representatives from the Ministry of Economy and Finance has also been formed.

The swift implementation of a deposit insurance scheme, initially through low premiums and low coverage to lighten the burden of financial institutions, could benefit the Cambodian banking consumers and contribute to the stability of the financial system.

With firm commitment from the authorities, we foresee the imminent establishment of a deposit protection scheme in Cambodia.