Central banks adjust monetary policy instruments, most notably short-term interest rates, to influence households’ and firms’ borrowing, spending, and investment decisions, with the aim of stabilizing inflation and supporting growth. However, these policy actions only work if they are effectively transmitted through the financial system, namely banks and capital markets. Recent analysis by AMRO shows that the monetary policy transmission in the Philippines remains delayed and incomplete, especially through bank lending and the long end of the government bond market.

Credit channel transmission remains delayed and limited

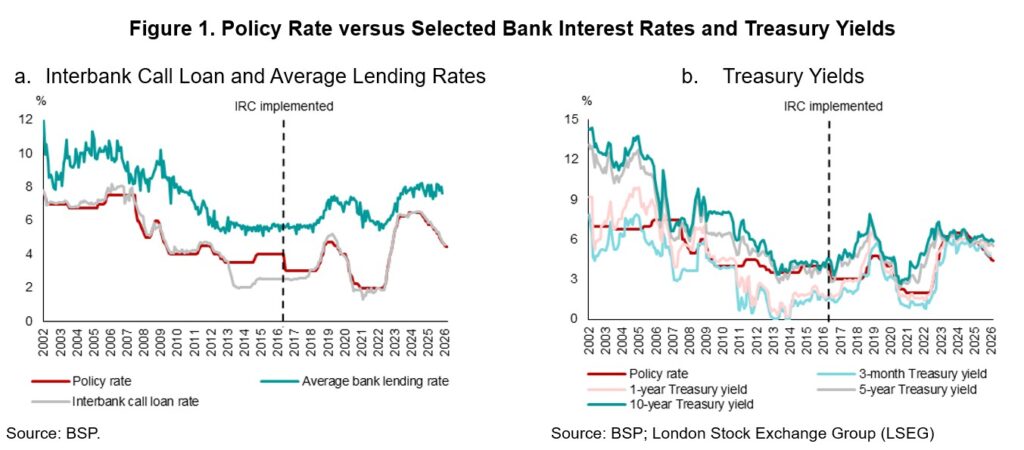

The analysis finds that the Bangko Sentral ng Pilipinas (BSP)’s policy rate has become a reliable anchor for short-term financial conditions. Short-term market rates, such as the interbank call loan rate and short-term (three-month and one-year) Treasury bill yields, now respond more quickly and align more closely with the BSP’s policy decisions. This improvement has been particularly evident since the adoption of the Interest Rate Corridor (IRC) in June 2016.

However, transmission to banks’ interest rates remains both delayed and limited. Lending rates still show an average pass-through of only about 57 percent of changes in the policy rate (Figure 1a). The stickiness is most pronounced in consumers loans and loans to small, and medium-sized enterprises (SMEs), where transmission is weaker than for corporate lending. This partly reflects weaker competition in these segments, as well as higher risk premiums charged by banks amid insufficient credit risk information.

Bond market transmission weakens beyond the short end

In the government bond market, the timeliness and strength of monetary policy transmission vary markedly across maturities. At the short end of the yield curve, policy rate changes are reflected relatively quickly, typically within two months. By contrast, transmission to longer maturities, such as ten-year government bonds, takes more than two months. Responsiveness also tends to diminish as bond maturity lengthens, particularly during a tightening cycle (Figure 1b).

Although long-end yields are influenced by factors beyond policy rates, this muted response at the longer tenors reflects, above all, limited market depth. A deep and liquid government bond market is essential for effective price signaling, especially when the BSP raises the policy rates. Yet the Philippine bond market remains relatively shallow, constraining this transmission mechanism.

Banks and contractual savings institutions hold about 75 percent of outstanding local-currency government debt, while foreign participation is only about five percent. This is well below Malaysia (21 percent), Indonesia (14 percent), and Thailand (nine percent), where broader investor bases support liquidity and price discovery. With trading volumes in long-term bonds remaining modest, policy signals struggle to translate into clear movements in long-dated yields.

Structural reforms for credit information system and bond market liquidity

Improving monetary policy transmission in the Philippines requires targeted structural reforms in both the bank credit channel and the capital market channel.

On the banking side, strengthening credit information systems can reduce information asymmetry, reflect more accurate risk-based pricing, and encourage wider adoption of floating-rate loan products. This would allow lending rates to respond more effectively to changes in monetary policy. The BSP’s introduction of the Credit Risk Database Philippines, which generates credit scores and default probabilities using anonymized financial and non-financial data, is an important step forward. Moreover, credit information systems should be more deeply integrated into banks’ credit assessment and lending practices, especially for consumers and SMEs, where transmission is often weakest.

On the capital market side, reforms should focus on deepening liquidity and broadening the investor base for government securities. Stronger market depth would strengthen price discovery and enhance the responsiveness of long-term yields to policy signals. Channeling more domestic savings—such as through personal equity and retirement accounts, or investments by government-owned and government-controlled corporations—to long-term capital markets could achieve this objective.

Meanwhile, attracting greater foreign participation would further deepen capital markets. Measures such as streamlining tax-refund procedures for foreign investors, adopting global settlement standards, advancing inclusion in the JP Morgan Emerging Market Bond Index, and linking the Philippine Stock Exchange with regional markets under the Asian Bond Market Initiative could all play a meaningful role.

Monetary policy transmission in the Philippines remains constrained by structural bottlenecks rather than policy intent. Further reforms in credit scoring, bank lending practices, and long-term capital market development are needed to ensure policy decisions are transmitted more effectively to the real economy, and to support a more inclusive and effective monetary policy framework in the years ahead.