Since 2024, property prices in Seoul have soared. Policymakers have once again stepped up efforts to cool the housing market, aiming to reduce financial stability risks stemming from rising household leverage. But with prices remaining persistently elevated, a key question is emerging: are Korea’s macroprudential tools still as effective as they once were, or is their impact beginning to fade?

Recent developments suggest that while policy tightening can still ease demand pressures, its effectiveness over a prolonged period may be diminishing.

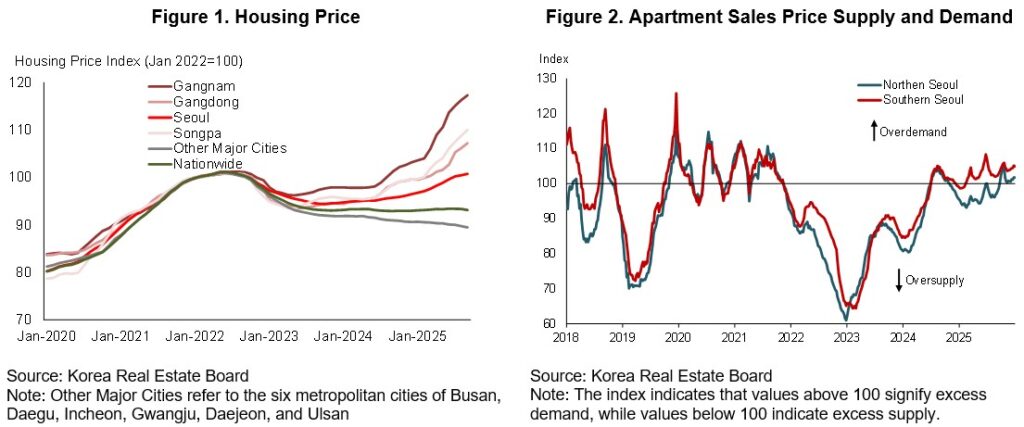

A surge driven by demand and expectations

Housing prices in Seoul have climbed even amid domestic political uncertainty and external headwinds over the past two years. The divergence within the country has been striking: prices in key districts such as Gangnam, Seocho, and Songpa have risen sharply, while those outside the Seoul Metropolitan Area (SMA) remained lackluster.

Several forces are at play.

Easing financial conditions, including lower interest rates and buoyant equity markets, have expanded borrowing capacity. At the same time, homebuyers’ preferences have increasingly shifted toward Seoul, reinforcing demand in already supply-constrained districts. Expectations of continued price appreciation have further fueled this dynamic, creating a self-reinforcing cycle of rising demand and prices.

Stepping-up policy tightening efforts

In response, authorities have deployed a series of measures to curb price increases.

On the demand side, macroprudential tightening has focused on credit conditions: tighter mortgage limits, lower loan-to-value (LTV) ratios, and expanded debt-service-ratio (DSR) requirements. Additional measures, such as land transaction permits and minimum owner-occupancy rules, aimed to curb speculative demand.

At the same time, policymakers have sought to address supply constraints by announcing large-scale housing construction plans in the SMA to ease structural shortages.

This reflects a familiar policy mix: restraining demand in the short term while expanding supply over the medium term.

What the evidence suggests: waning effectiveness

As discussed in AMRO’s 2025 Annual Consultation Report on Korea, these measures can help dampen housing demand in the short term, particularly in districts experiencing steep price increases, while containing pressures elsewhere in the SMA.

From a longer horizon, however, the picture is more nuanced.

Empirical analysis of past tightening episodes suggests that each measure reduces house prices by about 0.1 percent over two years, a modest effect relative to the scale of recent gains. More importantly, the impact appears to have weakened over time. Before 2017, similar measures had nearly twice the effect.

This points to a broader challenge in macroprudential policy: diminishing returns when supply constraints persist.

Behavioral adaptation also plays a role. As borrowing conditions tighten, households increasingly turn to alternative funding sources – such as family loans or non-bank financing – blunting the effectiveness of traditional credit-based tools.

Not all tools are equal

Among the main instruments, LTV-based measures appear to have more persistent effects than DSR tightening.

Lower LTV ratios tend to exert a stronger and longer-lasting dampening effect on house prices, although their impact has also declined over time. By contrast, DSR tightening appears to have a shorter-lived influence, with effects fading beyond the first year.

Even the more effective tools, however, have a relatively small impact compared with the scale of recent price increases. This underscores the growing difficulty of relying on macroprudential tightening alone to stabilize the housing market.

The broader implication is clear: macroprudential tools still work, but less reliably than before.

Repeated use of similar instruments has encouraged circumvention and adaptation by savvy homebuyers, eroding their marginal impact. While combining tools can strengthen effectiveness, there are limits to how far tightening can go, especially when underlying demand remains strong.

The missing piece: supply

Cooling Seoul’s housing boom remains a complex challenge. If demand-side tools are losing traction, policy priorities will need to recalibrate.

Expanding housing supply, particularly in high-demand areas such as the SMA, is becoming critical. Easing restrictions on reconstruction and redevelopment in sought-after districts could help, as could selectively releasing greenbelt land for housing development.

More fundamentally, a broader, multi-pronged strategy will be needed. Policies in education, healthcare, and transport all shape where people choose to live—and why demand continues to concentrate in the capital region.

Without such measures, each new round of macroprudential tightening is likely to deliver diminishing results.