A version of this article was first published in China Daily on November 23, 2025.

For decades, Hong Kong, China stood as Asia’s quintessential shopping paradise—a place where luxury boutiques lined every major street, global brands launched their flagships, and visitors from across the region filled malls and markets. The city’s retail success was inseparable from its rise as a financial and tourism hub. But that golden age has faded into something more complex.

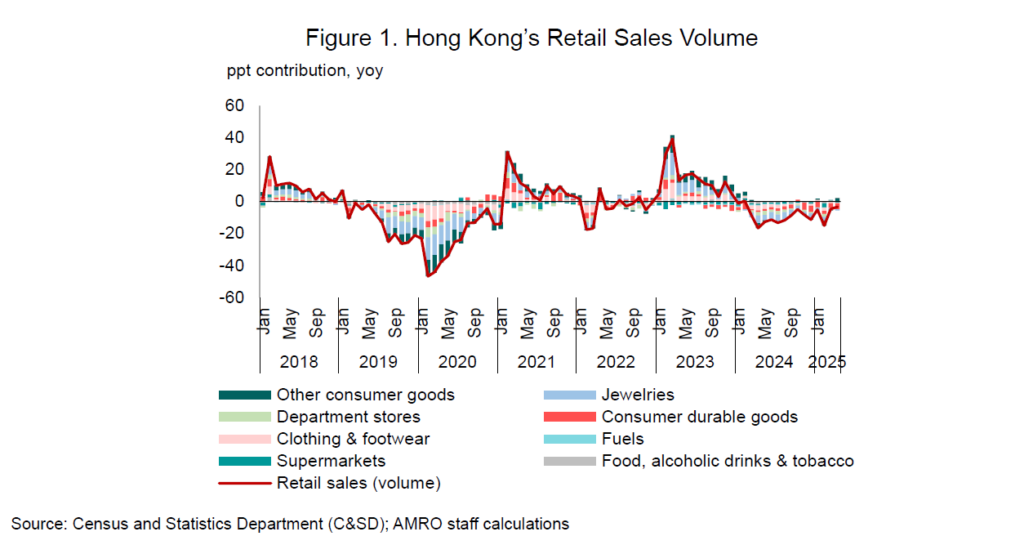

Since reopening after the pandemic, Hong Kong’s retail sector has experienced a gradual recovery rather than the sharp rebound many had anticipated. As of April 2025, retail sales had contracted for 14 consecutive months (Figure 1), with high-end segments such as apparel, jewelry, and consumer durables taking the hardest hit. Yet, this slowdown does not necessarily spell the end of Hong Kong’s retail dominance—it signals the need for reinvention.

A long history of resilience

Hong Kong’s retail sector has always been remarkably resilient. From the 1980s through the early 2000s, retail sales expanded at double-digit rates. Even major shocks—the Asian Financial Crisis, SARS, and the Global Financial Crisis—caused only temporary disruptions. Recovery was often swift and robust, powered by the city’s openness, efficiency, and influx of Mainland Chinese tourists.

But the shocks of the past decade were of a different magnitude. Slower global growth in the mid-2010s, social unrest, and finally the pandemic hit both supply and demand in ways unseen before. Even after borders reopened in 2023, retail recovery lagged behind broader economic growth. The structural forces reshaping consumption patterns are now far more enduring.

Five key drivers shaping retail

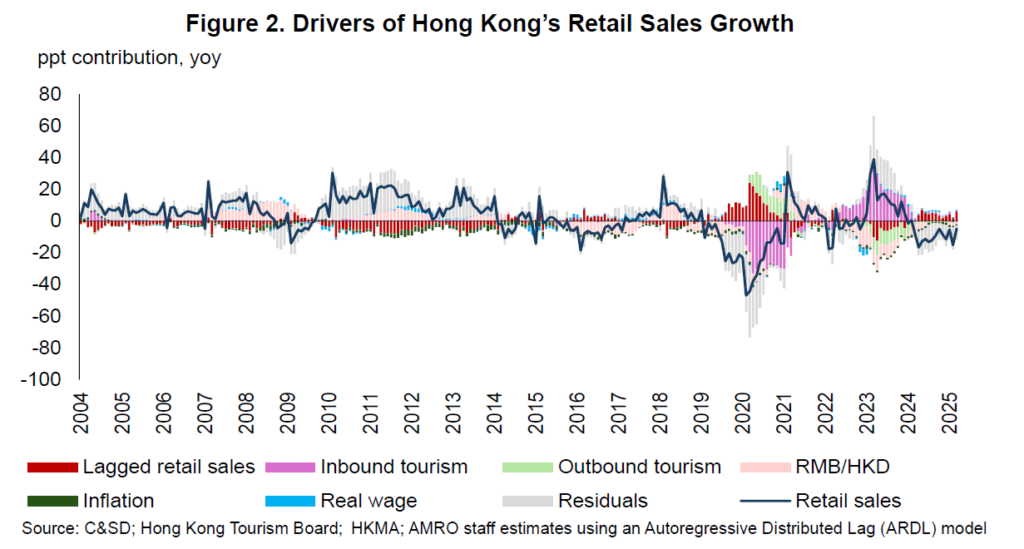

A recent analysis by AMRO economists identified five key factors that shaped the city’s retail performance: inbound and outbound tourism, real wages, the Hong Kong dollar exchange rate, and inflation (Figure 2).

Tourism was the single most important driver. Before 2020, spending by Mainland Chinese visitors accounted for a large share of retail turnover, especially in luxury goods. When borders closed, that lifeline vanished. Since 2023, tourism has picked up, but the behavior of travelers has changed. Many tourists now prefer experiences over shopping, while others are more cautious amid an uncertain global economic outlook.

Meanwhile, outbound tourism surged. With a strong Hong Kong dollar and greater cross-border convenience, many residents now spend their leisure budgets abroad—often just across the border in Shenzhen, where dining, wellness, and retail options have proliferated. This shift has diverted significant household spending away from local retailers.

The exchange rate also worked against Hong Kong’s competitiveness. The Hong Kong dollar’s appreciation against the renminbi since 2016 has eroded the city’s price advantage, making it more expensive for Mainland visitors.

Inflation added further strain. Rising rents and utility costs ate into purchasing power, discouraging discretionary spending. However, one bright spot has been rising real wages. Strong labor market conditions in 2023-2024 boosted incomes and supported domestic consumption, providing a crucial buffer for the sector.

Policy push: From shopping hub to experience hub

The Hong Kong government has moved quickly to respond. Working closely with industry stakeholders, it has rolled out initiatives to boost inbound tourism, retain local spending, and cushion the effects of outbound shopping. These include expanding the Individual Visit Scheme to more Mainland cities, curating a full calendar of mega-events, and revitalizing cultural districts and waterfronts.

Authorities are also promoting the “silver” and “green” economies, supporting both luxury brands and local creative start-ups. Retail vouchers, loyalty programs, and themed shopping festivals have been launched to encourage residents to shop locally. The broader strategy is clear: to reposition Hong Kong as a premier experiential retail destination—where technology, art, and culture intersect.

Encouraging signs are emerging. Flagship stores from major brands such as Prada, Dior, and, Hermes are reopening, signaling renewed optimism in the retail landscape. The city’s rising position in global city rankings and the strong turnout at recent large-scale events—from Art Basel to Clockenflap—underscore Hong Kong’s enduring appeal as a vibrant urban experience.

Charting the next phase

Still, Hong Kong’s retail sector cannot rely on a return to its pre-pandemic model. Structural changes in consumer preferences, digital shopping habits, and intensifying regional competition mean the future must look different. The challenge is not merely to revive retail; it is to reinvent it.

Four priorities stand out:

1. Strengthen tourist appeal. Diversify retail offerings beyond traditional luxury and deepen experiential elements—from curated neighborhoods and immersive art spaces to smart retail technology. Seamless transport and efficient border crossings can make every visit frictionless.

2. Encourage local spending. Incentivize residents to “shop local” through loyalty programs, digital transformation, and collaborations between local designers and international brands. Retail should be seen not just as consumption, but as part of community life and cultural expression.

3. Boost household spending power. Sustained wage growth, productivity gains, and targeted support for lower-income households will expand the domestic consumer base and create a more inclusive retail ecosystem.

4. Build sectoral resilience. Integrate retail with tourism, logistics, and digital platforms to create new business models that can adapt quickly to external shocks. Data-driven analytics, online-offline integration, and regional partnerships will be key.

A reinvention story in progress

Hong Kong’s retail landscape is unlikely to return to the breakneck expansion of earlier decades. However, with thoughtful policy, creative energy, and cross-sector collaboration, Hong Kong can once again be a leading attraction in the region—not merely as a shopping haven, but as Asia’s premier experiential retail capital, where every purchase is part of a story, and every visit an experience to remember.