Despite persistent global headwinds, the Malaysian ringgit appreciated against the US dollar during the first five months of the year, extending its strong performance from 2025 even as most regional currencies weakened. These earlier gains provided some buffer against recent depreciation pressure amid rising election-related uncertainty.

Strong domestic fundamentals and the global AI capex boom have supported the ringgit. Beyond these cyclical factors, Malaysia’s foreign exchange (FX) policy framework has also encouraged sustained two-way flows through the domestic market, contributing to the currency’s stability.

Liberalizing to stabilize

While some economies have reacted to market pressures by tightening selected FX rules, curbing outflows, or drawing on reserves to support their currencies, Malaysia has taken a more facilitative approach. A key example is the full rollout of the Qualified Resident Investor (QRI) program in 2025.

Under the QRI framework, qualified and enrolled resident corporates may undertake direct investment abroad without prior approval from Bank Negara Malaysia (BNM). Investment amounts are capped at eligible foreign currency funds that have been repatriated and converted onshore. The framework gives firms greater flexibility in managing overseas investments, while promoting the recycling of foreign income through Malaysia’s financial system.

The QRI program forms part of a broader series of FX liberalization measures introduced over the years. These include relaxing FX conversion requirements for exporters, broadening hedging flexibility for resident and non-resident market participants, and expanding access to Malaysia’s domestic market for multilateral development banks and qualified non-resident development finance institutions.

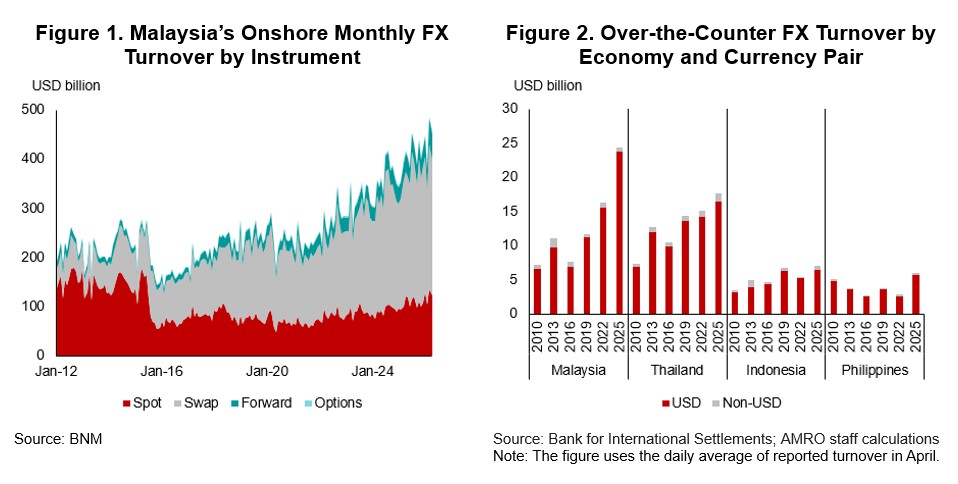

Collectively, these reforms have helped deepen Malaysia’s domestic financial markets while providing businesses and investors with greater flexibility to manage cash flows and hedge FX risks, as reflected in the increased use of onshore FX swaps over the years (Figure 1).

More importantly, deeper and more liquid two-way markets are better able to absorb shocks and reduce one-sided pressure on the ringgit. When market participants can move funds in both directions and manage risks efficiently, the domestic FX market becomes more resilient. In this way, greater openness can reinforce stability rather than undermine it.

Adapting to a changing landscape

Looking ahead, Malaysia’s FX policy framework should continue to evolve alongside changes in the global financial landscape. One important trend is the region’s growing push to expand the use of local currencies in cross-border trade and investment, even as the US dollar remains the dominant vehicle currency in regional transactions (Figure 2).

To support this shift, BNM has worked with its counterparts in Indonesia and Thailand to enhance the Local Currency Transaction Framework. The revised framework harmonizes regulatory guidelines and facilitates the wider direct settlement of cross-border transactions in local currencies. Such initiatives can help reduce transaction costs, diversify funding and settlement options, and strengthen regional financial integration.

At the same time, financial innovation is reshaping the global payments and financial ecosystem. Digital forms of money and assets could alter the channels through which cross-border flows move and are monitored, potentially reducing the effectiveness of traditional FX regulations.

In this context, initiatives such as the Digital Asset Innovation Hub provide an important platform for assessing the operational and regulatory implications of digital assets. By allowing regulators and market participants to explore emerging technologies in a controlled environment, such initiatives can help inform future refinements to Malaysia’s FX policy framework.

The challenge for policymakers is to strike the right balance between openness and stability. Greater financial openness can deepen domestic markets, improve capital allocation, and enhance market efficiency. At the same time, it can increase exposure to volatile capital flows and external shocks.

Malaysia’s ability to manage this trade-off reflects enabling conditions, including ample reserves, sound macroeconomic fundamentals, and a carefully sequenced approach to reforms. These foundations have allowed policymakers to pursue liberalization gradually while maintaining confidence in the domestic financial system.

As the global financial landscape continues to evolve, Malaysia’s experience offers an important lesson: FX liberalization and financial stability need not be competing objectives. When supported by strong fundamentals, effective regulation, and prudent safeguards, greater openness can strengthen rather than weaken market resilience.

Malaysia should therefore continue its gradual and facilitative approach to FX liberalization, supported by strong prudential safeguard that preserve the efficiency, soundness, and competitiveness of its financial markets.