This article first appeared in The Edge Malaysia on July 2, 2026.

The global race to build artificial intelligence (AI) capabilities is redrawing Asia’s investment map, and Malaysia stands out as one of the region’s biggest beneficiaries. Surging demand for computing power, cloud services, and data storage is rapidly transforming the country into a regional data center hub. But the pace of expansion is also exposing structural constraints that will determine how durable this boom proves to be.

The rise of AI applications—particularly large language models (LLMs)—has fundamentally changed demand for digital infrastructure. Training and operating these models require enormous computing capacity, while broader cloud adoption continues to drive demand for data storage. Together, these trends have triggered a global wave of data center investment, with Malaysia emerging as an increasingly attractive destination.

A confluence of advantages

Several structural advantages underpin Malaysia’s appeal.

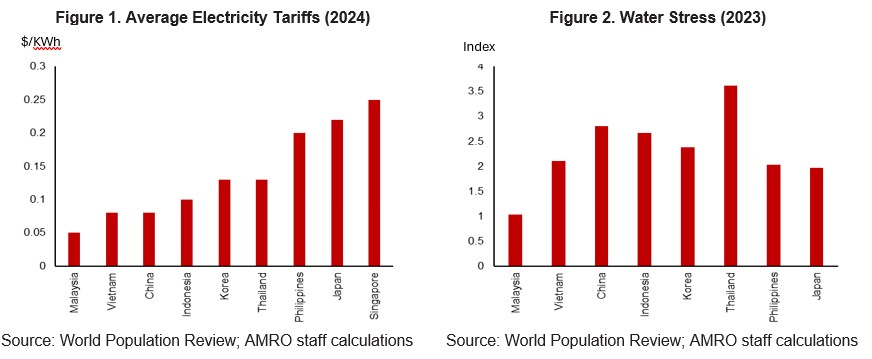

One of the most important is its relatively low electricity cost. Data centers operate around the clock and consume large amounts of power, making affordable and reliable energy supply a critical consideration. While elevated global energy prices stemming from the Middle East conflict may exert upward pressure on electricity tariffs, Malaysia remains cost competitive relative to many regional peers and advanced economies (Figure 1). The country also maintains a comfortable electricity reserve margin.

At the same time, abundant rainfall and relatively low pressure on water resources (Figure 2) strengthen Malaysia’s suitability for water-intensive cooling systems used in modern data centers.

Geography further reinforces the country’s competitiveness. Located outside the Pacific Ring of Fire, Malaysia faces lower risks from earthquakes and other natural disasters that could disrupt operations. Equally important is proximity to Singapore, one of Asia’s leading digital connectivity hubs. Singapore’s extensive network of undersea cables enables operators in neighboring Johor to access global digital infrastructure efficiently while benefiting from lower operating costs.

Johor has consequently become the focal point of Malaysia’s data center expansion. A key catalyst was Singapore’s temporary pause on approvals for large-scale data center developments between 2019 and 2022, which prompted investors to look across the Causeway. While Klang Valley historically hosted most of the country’s facilities, Johor now accounts for around 80 percent of Malaysia’s operational data center capacity, driven largely by hyperscale operators serving cloud and AI demand.

Nationally, total data center capacity is projected to increase from around 0.9–1GW in 2025 to as much as 3–4GW by 2029.

Government policy has also supported the sector’s growth. Through initiatives such as the Digital Ecosystem Acceleration (DESAC) scheme and Malaysia Digital (MD), authorities have introduced tax incentives and investment allowances to attract digital infrastructure projects. Malaysia has also developed a relatively comprehensive and coordinated regulatory framework covering site planning, sustainability requirements, renewable energy procurement, and strategic development priorities. Compared with regional peers, this more systematic approach has strengthened investor confidence.

Challenges on the horizon

Rapid expansion, however, is creating new pressures.

Although Malaysia is expanding electricity capacity, particularly through new gas-powered projects, demand growth could outpace supply in some locations. Reflecting these concerns, Malaysia began restricting new non-AI data center investments in February 2026 because of their high electricity and water requirements.

Water consumption presents a major challenge. Cooling systems for high-performance servers require substantial volumes of water, with a 100MW facility consuming around 4.2 million liters daily. As data center clusters continue to expand, pressure on local water infrastructure could intensify, increasing the importance of sustainability standards and resource-efficient technologies.

Questions also remain about the scale of domestic economic spillovers. During construction, much of the equipment used in Malaysian data centers—including servers, cooling systems, networking hardware, and integrated racks—is imported. As a result, only a limited share of value added is captured locally, with most domestic benefits concentrated in construction activity.

The operational phase offers greater opportunities. Spending on utilities, leasing, maintenance, and support services generates higher domestic value added, while data centers can support growth in ICT services exports such as cloud computing, hosting, and data processing. Over time, deeper integration into higher value-add digital activities—including software development and enterprise services—could significantly increase the sector’s contribution to economic growth.

Employment effects are similarly mixed. Construction generates substantial temporary employment, but operational facilities require relatively small workforces, often employing only 30–50 full-time staff. At the same time, the industry faces shortages of specialized talent in areas such as IT infrastructure management and environmental controls, while competition for skilled workers with Singapore continues to intensify.

Ensuring sustainable growth

Malaysia has successfully positioned itself as a key destination in Asia’s digital infrastructure expansion, supported by favorable geography, competitive costs, and proactive policymaking.

Sustaining that momentum, however, will require more than attracting investment. The next phase of growth will depend less on how many gigawatts are added and more on what develops around them: deeper domestic supply chains, a stronger talent pool, and greater participation in higher-value digital activities.

As economies across the region compete to host the next wave of AI infrastructure, Malaysia’s experience highlights an important lesson. Attracting capital is only the first step. The greater challenge is converting digital infrastructure into durable, locally anchored growth while ensuring resource sustainability, supply-chain development, and human capital keep pace with expansion.