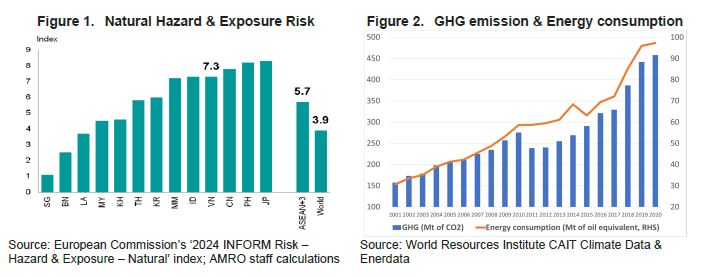

Vietnam is one of the world’s most hazard-prone countries to climate change risks. The country faces high natural disaster risk levels, fourth highest in the ASEAN+3 region and far above the world average (Figure 1).

Its geographical features, especially the concentration of economic activities along its long and densely populated coastline and numerous transboundary river basins, which are exposed to typhoons, sea-level rise and floods, make the country highly vulnerable to extreme weather induced by climate change.

Moreover, Vietnam has witnessed a marked increase in greenhouse gas (GHG) emissions as well as energy consumption due its rapid economic growth. Its GHG emissions and electricity consumption have grown about threefold over the last two decades and will continue to increase in the next few decades in line with rapid industrialization and urbanization (Figure 2).

Against this backdrop, how should Vietnam further strengthen its climate resilience, given that it has a long way to go?

Policy recommendations

The country’s ongoing efforts to strengthen climate adaptation measures are encouraging. These measures include industrial and urban development strategies, early warning systems to monitor and predict hazards, and hard infrastructure such as dikes and sea walls to reduce severe coastal and riverine erosion.

Going forward, adaptation strategies should focus more on the country’s most vulnerable locations and sectors, particularly low-lying coastal areas and flood-prone river basins.

In May 2023, Vietnam approved the Power Development Plan 8 (PDP8) to phase out coal power by the 2040s. However, accelerating the country’s transition to clean energy can exacerbate power shortages and fuel price rises, and cause a myriad of problems for vulnerable sectors, especially energy-intensive manufacturing.

In this context, climate mitigation measures should be developed and implemented early and over a period of time to minimize transition risks toward a low-carbon economy and scale up deployment of green technologies. It is also important to establish support schemes for the vulnerable groups and sectors in consideration of distributional impact of the transition cost to a low-carbon economy, including power shortages and fuel price rises.

Furthermore, the introduction of carbon pricing mechanisms, stricter emission standards, or the phasing out of coal power, can affect the profitability and competitiveness of energy-intensive businesses. In particular, a carbon trading market, including an Emissions Trading System (ETS) and a carbon credit mechanism to measure the impact made by companies, individuals, and governments, is touted as the most efficient strategy to fulfill the country’s COP26 commitments.

The green economy is becoming a key pillar to fuel growth and address energy constraints in an integrated way. Multinational companies and consumers are shifting toward low-carbon markets and products. The government should continue to accelerate the “Vietnam Green Growth Strategy (VGGS)”, which aims to improve the efficiency of the entire economy and drive growth in a sustainable manner. In particular, more attention should be paid to attracting FDIs by providing favourable conditions for green industries.

The country should also advance green technologies across all industrial infrastructure. After all, economies that fail to accelerate the low-carbon technology deployment and the energy efficiency improvement would be susceptible to stranded fossil-fuel based assets and investments.

To that end, Vietnam can speed up the deployment of carbon capture, utilization and storage (CCUS) which enables industrial and power facilities to operate with substantially reduced GHG emissions.

The National Energy Masterplan (NEMP), approved in August 2023, aims to achieve a CCUS capacity of about 1 million metric tones per year (mt/year) by 2040 and 3-6 million mt/year by 2050 from industries and power plants. Going forward, Vietnam has the potential to develop a CCUS hub in the region, alongside Indonesia, Singapore, Thailand, Malaysia and Brunei Darussalum.

Mobilizing the private sector is crucial in raising the much needed investment. The Direct Power Purchase Agreement (DPPA) piloted in 2022 enables corporations to procure clean energy power directly from private generators for the first time and is an important step forward.

In addition, the government can look at strengthening financial resources, technology and capacity building under bilateral and multilateral international cooperation mechanisms, especially within the framework of United Nations Framework Convention on Climate Change (UNFCCC).

To conclude, while there are many pockets of opportunities for Vietnam to strengthen its climate resilience, the government must implement its adaptation and mitigation measures at a faster pace, with careful consideration of the distributional implications to the vulnerable groups. In addition, more attention should be paid to the costs and sources of funding of the climate change-related strategies since the scale and the timing of the financial needs are uncertain in the long term.