This article was first published as an op-ed in The Jakarta Post on July 27, 2023.

Indonesia may not be an aging society yet, but the country is expected to age at a faster pace due to declining fertility rate and rising life expectancy. Hence, pension reforms are crucial to cope with an aged society in future. A strengthened pension system is also an important source of financing for Indonesia’s long-term development needs and to provide support for the domestic capital market in times when foreign investors turn risk averse.

Efforts to reform the Indonesian pension system were implemented as early as the 1990s with the issuance of Law No. 3/1992, also known as the Jamsostek Law, to mandate all formal-sector workers to contribute to the old-age savings scheme.

In 2004, the issuance of Law No. 40/2004, also called the National Social Security System Law or SJSN Law, expanded the old-age savings scheme to cover informal-sector workers, while a new pension scheme was introduced for formal-sector workers.

More recently, the Omnibus Law on the Development and Strengthening of Financial Sector was approved by parliament in 2022. This legislation is aimed at reforming the national pension system and deepening domestic financial markets in Indonesia.

Understanding Indonesia’s pension system

The pension system in Indonesia consists of mandatory and voluntary earnings-related schemes. Under the mandatory contribution program, several pension schemes are available in the country. The mandatory old-age savings scheme for all private-sector workers and the pension scheme offered to only private formal-sector workers are managed by a public entity known as BPJS Ketenagakerjaan (formerly Jamsostek). Separately, pension schemes for civil servants, and police and military officers are managed by state-owned companies, Taspen and Asabri, respectively.

Voluntary pension schemes are offered by employers to their employees or by financial institutions for (self-employed) individuals. These voluntary schemes are managed mostly by banks and insurance companies.

Relatively low ranking in the region

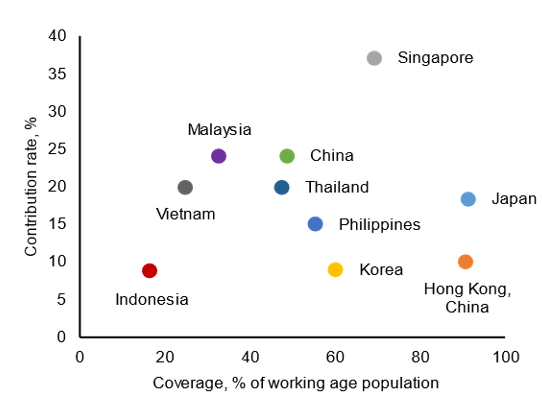

Indonesia’s mandatory pension system is modest in coverage and size, compared with fellow economies in the ASEAN+3 region. Only about 30.7 million, or 16.5 percent of the working-age population, have actively participated/contributed to the mandatory old-age savings scheme. This is low compared to ASEAN+3 peers, mainly due to Indonesia’s large informal sector and a lack of retirement financial awareness.

Mandatory Pension Coverage and Contribution Rate

A low contribution rate has also led to Indonesia’s small pension fund size. BPJS participants contribute 8.7 percent of their monthly income to its old-age savings and pension funds, which is among the lowest in ASEAN+3.

BPJS’s total assets stood modestly at IDR629 trillion in Dec 2022, or about 3.3 percent of GDP. This has been worsened by current regulations that allow participants to withdraw funds before retirement, eroding BPJS funds.

By comparison, Malaysia’s Employment Provident Fund (EPF)’s assets amounted to 65.5 percent of GDP and Singapore’s Central Provident Fund (CPF)’s assets were about 85.3 percent of GDP in 2022.

The way forward

Ongoing demographic changes underscore the importance of reforming Indonesia’s pension system. While it is still one of the youngest countries in the region, Indonesia has entered an aging phase with people aged 65 years old and above accounting for 7 percent of the total population. It is projected to become an aged society by 2050 when the ratio surpasses 14 percent, and super-aged by 2070 when the ratio reaches 20 percent.

To prepare for an aging population, Indonesia has raised the retirement age from 55 by one additional year every three years since 2014 and will continue to do so until 2043 when it reaches 65. The Omnibus Law on Development and Strengthening of Financial Sector has sought to redesign the mandatory pension schemes to prevent participants from fully withdrawing their pension funds before the retirement age.

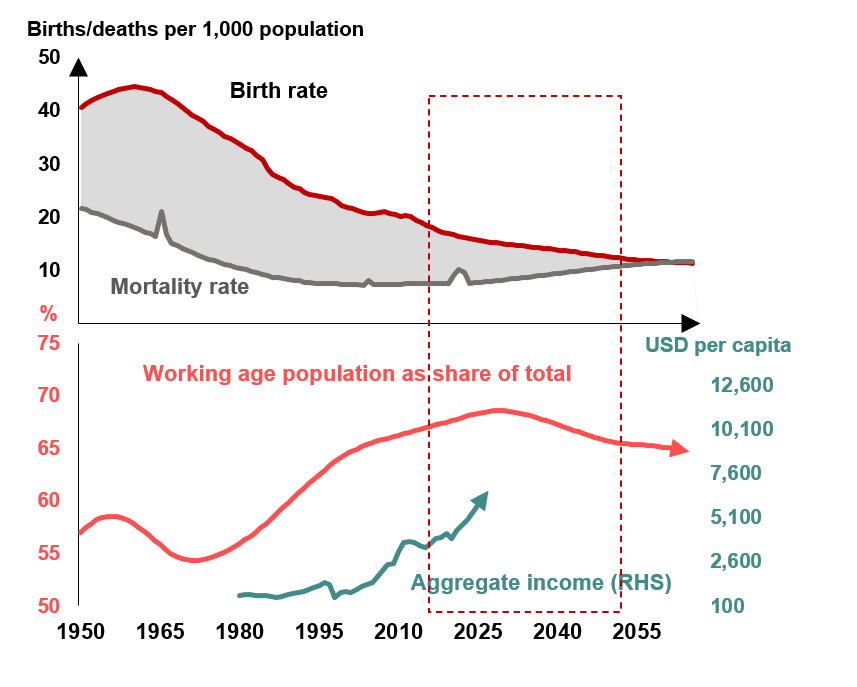

Demographic Dividend and Aggregate Income

Source: Source: UNDP; IMF; national authorities; CEIC; AMRO staff calculations

Note: The red-dotted frame indicates the demographic dividend window, based on UNDP projections for the medium variant scenario for Indonesia. Aggregate income is measured as nominal GDP per capita in USD terms, reported by the IMF.

Going forward, coverage of the pension system could be further expanded to cover more formal and informal sector workers, with continued efforts to raise awareness among informal-sector workers. Raising the mandatory contribution rate will also be necessary to help enhance pension adequacy and sustainability.

Making early adjustments to the contribution rate, especially before or during the demographic dividend window, would help pension funds to accumulate assets at a faster pace and avoid the need to make drastic adjustments after the window is closed, as suggested by other countries’ experience.

Indonesia is now enjoying its demographic dividend with the share of the working-age population expected to peak around 2030. Therefore, timely actions on pension reforms are urgently needed.