As global finance becomes increasingly shaped by geopolitical tensions and market volatility, enhancing financial resilience has become a priority across economies. While the US dollar continues to anchor trade and finance—and remains the dominant global reserve currency—recent episodes of market stress have underscored the importance of credible alternatives and complementary liquidity backstops.

Against this backdrop, Europe’s efforts to strengthen the international role of the euro—often framed as a “Global Euro” agenda—offer useful reference points for ASEAN+3. Importantly, this agenda reflects a broader strategic direction, rather than any single policy instrument.

The “Global Euro” as a strategic direction

Europe has long sought to enhance the euro’s global standing through deeper market integration, advances in green and digital finance, and greater operational utility. In the current environment of heightened geoeconomic fragmentation, these efforts have taken on greater strategic urgency.

Recent initiatives—including progress toward a Savings and Investment Union to deepen capital market liquidity, alongside developments in digital euro and payment systems—reflect a broader push to strengthen the euro’s resilience, usability, and international appeal. In this context, calls for a “global euro moment” highlight a growing recognition that currency internationalization increasingly depends not only on economic scale, but also on institutional credibility and operational readiness.

EUREP and liquidity diplomacy: Building a rules-based backstop

With this broader strategy, the European Central Bank’s (ECB) enhancement of the Eurosystem Repo Facility for Central Banks (EUREP) is a notable development. EUREP is not the “Global Euro” itself, but a concrete instrument that supports this ambition by strengthening the euro’s liquidity backstop.

Originally introduced as a temporary pandemic-era facility for a limited group of non-euro area central banks, EUREP is now being transformed into a permanent standing facility with expanded global access from the third quarter of 2026. Under the enhanced framework, eligible central banks—subject to AML/CFT requirements—can access euro liquidity of up to EUR 50 billion by providing high-quality euro-denominated collateral.

This evolution marks a shift toward a more institutionalized and rules-based approach to liquidity provision. Comparable in function to the US Fed Reserve’s FIMA Repo Facility, EUREP enables the ECB to act as a predictable liquidity provider. In doing so, it adds a proactive dimension of “liquidity diplomacy”—reducing the risk of disorderly asset sales during periods of stress, supporting the stability of euro-denominated markets, and reinforcing confidence in the euro as an international reserve asset.

Practical relevance for ASEAN+3: Enhancing optionality

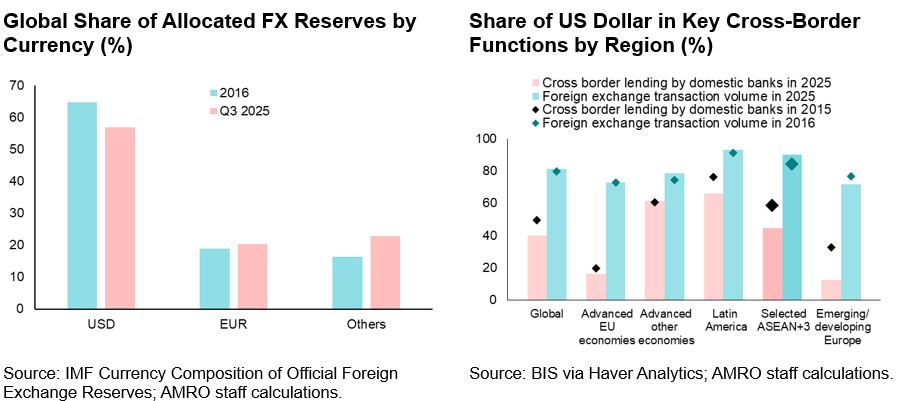

For ASEAN+3 economies, the expansion of EUREP has practical relevance. While the US dollar remains dominant in the region’s cross-border financial systems—as noted in the ASEAN+3 Financial Stability Report (2024)—EUREP offers an important layer of optionality.

By enhancing the usability of euro-denominated reserve assets, the facility provides central banks with greater flexibility in liquidity management during periods of market stress. Rather than serving as a substitute for existing arrangements, it functions as a complementary buffer—strengthening resilience in a system heavily anchored to the US dollar.

Beyond liquidity: Strategic lessons for the region

Europe’s “Global Euro” ambition also offers broader lessons for ASEAN+3. The international role of a currency is not determined by economic size alone. It rests equally on policy coherence, deep capital markets, and, most importantly, institutional credibility.

As ASEAN+3 continues to strengthen its financial safety net, three areas stand out:

- Fortifying the CMIM: Enhancing the operational readiness and analytical credibility of the Chiang Mai Initiative Multilateralisation (CMIM) will ensure it remains an agile and effective regional backstop against exogenous shocks.

- Deepening local capital markets: Further development and integration of regional bond markets can reduce structural over-reliance on external financing and the risks of sudden capital flow volatility. Initiatives such as the Asian Bond Markets Initiative (ABMI)—expected to evolve from 2027 with a broader scope beyond local currency bond markets while retaining bonds as its core focus and potentially expanding into a wider array of financial instruments to facilitate more efficient recycling of regional savings—remain central to this effort.

- Advancing payment connectivity: Strengthening cross-border payment linkages is a practical step toward greater financial autonomy. As digitalization reshapes global finance, efficient and interoperable payment systems will be essential for managing future shocks.

Conclusion: Credibility as the foundation of resilience

The euro’s international standing ultimately rests on institutional credibility—anchored in transparency, a rules-based framework, and confidence in policy implementation.

While contexts differ, the ECB’s evolving approach underscores a broader lesson: financial resilience is not only a matter of strategic intent, but of operational capability. EUREP illustrates how targeted instruments can reinforce that capability by strengthening confidence, usability, and stability.

For ASEAN+3, the key priority is clear. Enhancing resilience will depend not only on reinforcing regional frameworks such as AMRO and the CMIM, but also on ensuring these mechanisms are credible in practice, operationally ready, and capable of delivering timely and effective responses when needed. Ultimately, sustained efforts to build institutional credibility remain the essential foundation for deeper regional financial integration.