Korea’s shipbuilding industry has anchored the country’s export success for over half a century. From a government-nurtured heavy industry in the 1960s, the sector has grown into a global leader, specializing in technologically advanced vessels. Today, a cyclical rebound in global demand is restoring momentum, but a new set of structural challenges will shape its trajectory in the coming years.

From repair hub to global leader

Korea laid the foundations of its shipbuilding industry during the government-led industrialization drive of the 1960s and 1970s. The government identified shipbuilding as a strategic sector and backed it with concessional financing, tax incentives, and purpose-built infrastructure.

These efforts paid off. Within decades, Korea transformed from a modest ship repair hub into a world-leading shipbuilder. By the early 2000s, Korean yards had built a reputation for large, technologically sophisticated vessels—particularly container ships and gas carriers—fueled by the strong growth in global trade.

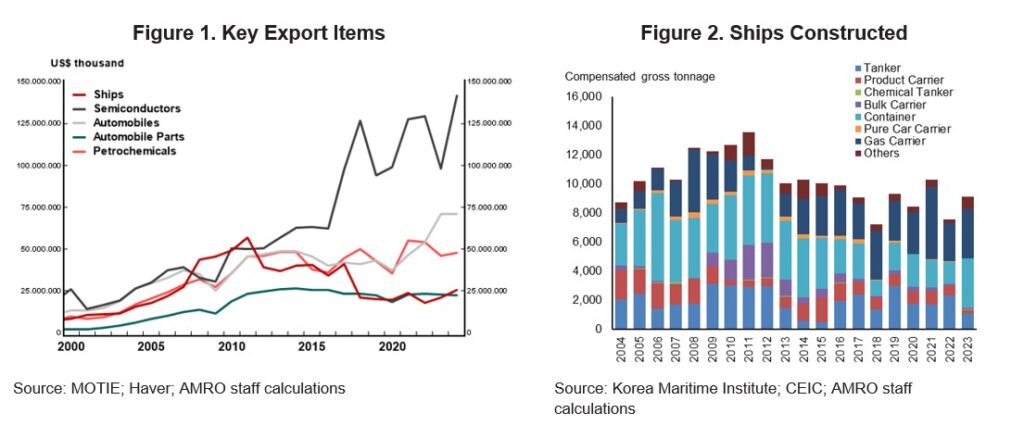

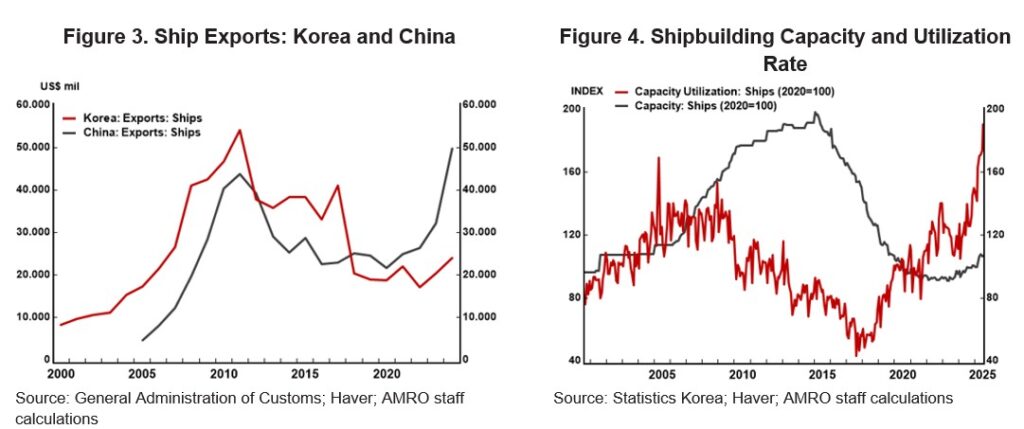

The industry reached a peak in 2011, when shipbuilding briefly surpassed semiconductors as Korea’s top export. Korean shipyards dominated the share of global orders for liquefied natural gas (LNG) carriers—high-value, technologically demanding vessels with limited global competitors.

Strategic pivot following global headwinds

The dominance came under strain in the 2010s. Slower global trade after the Global Financial Crisis weakened demand for new vessels. At the same time, China expanded its shipbuilding capacity aggressively, competing on both price and delivery speed.

As Chinese shipyards steadily gained market share, Korea’s ship exports came under pressure, resulting in a period of industry restructuring. Shipbuilding capacity contracted sharply as companies sought to restore financial viability and reposition themselves in an increasingly competitive global landscape.

Instead of competing on cost, the industry pivoted. The industry doubled down on high-value vessel segments—LNG and liquefied petroleum gas (LPG) carriers, alongside environmentally advanced vessels—where engineering capability matters more than cost. This strategic repositioning preserved Korea’s edge in specialized, high-margin markets.

Renewed momentum in global shipbuilding

Since 2020, the global shipbuilding market has entered a renewed upcycle. A post-pandemic rebound in global trade has lifted demand for maritime transport, which carries around 90 percent of global freight.

At the same time, tighter international environmental regulations—led by the International Maritime Organization—are accelerating fleet renewal. Shipowners are replacing old vessels with more fuel-efficient and lower-emission alternatives.

This trend plays directly to Korea’s strengths. New orders increasingly focus on dual-fuel vessels and next-general ships powered by cleaner energy sources such as ammonia or hydrogen. These require sophisticated design and engineering, supporting higher margins and reinforcing Korea’s positioning in high-value ship markets.

Geopolitics adds a further tailwind. Rising global tensions are prompting countries to modernize their naval fleets, creating new demand across both commercial and defense sectors.

New opportunities through international cooperation

International cooperation is opening new avenues. Recent collaboration with the US under the 2025 “Make American Shipbuilding Great Again” initiative could see Korean firms establish new shipyards in the US, modernize existing facilities, train the American workforce, and strengthen American shipbuilding supply chains.

Such cooperation allow Korean shipbuilders to diversify geographically while contributing to broader industrial collaboration between the two economies.

Key challenges on the horizon

Despite these opportunities, Korea’s shipbuilding faces several structural challenges. China remains the most prominent competitor. Its shipyards are rapidly narrowing the technological gap in high-value vessel segments while retaining cost advantages rooted in lower labor costs. Given the labor-intensive nature of shipbuilding, this cost differential is not easily overcome.

The green transition, for its commercial promise, brings its own pressures. Developing and scaling new propulsion systems, such as ammonia- or hydrogen-based engines, require significant investment in research, engineering capabilities, and supply chain development—well before commercial returns are fully realized.

Labor constraints add another layer of risk. Following large-scale layoffs in the early 2010s, the shipbuilding workforce has aged, and younger workers are reluctant to enter a sector long viewed as physically demanding. Without renewal, labor shortages could become a binding constraint.

From rebound to resilience

The current recovery offers Korea’s shipbuilding industry a window—but not a guarantee—of sustained leadership. The question is no longer whether demand will return, but whether the industry can adapt fast enough to structural change.

Sustaining Korea’s shipbuilding leadership will require action on several fronts. Continued investment in advanced vessel design and green technologies will be essential to stay ahead of competitors. At the same time, automation such as robotic welding can help offset labor shortages and lift productivity. Workforce development will be equally critical—increasing adoption of virtual reality (VR) and extended reality (ER) technology in workforce training can help accelerate skill acquisition. Together with targeted government support, these efforts will be crucial in ensuring Korea’s shipbuilding industry remains resilient and globally competitive in a rapidly evolving maritime landscape.

Korea’s shipbuilding story has always been one of strategic adaptation. From government-led industrialization to high-value specialization, each phase has required a shift in approach. If the industry can translate today’s cyclical upswing into long-term capability, it will not only navigate emerging challenges, but continue to define the future of global shipbuilding.